Liquidity

Liquidity in relation to Stress Tests – Insurance

While banks perform a maturity transformation, as a general rule liquidity risk plays a subsidiary role for insurance undertakings. However, it may become more significant for example in the case of natural catastrophes with accumulation risks, mass cancellations of policies or capital market crises. While reinsurers assume 30% of claims on average, delayed payments by reinsurers may lead to a short-term liquidity need.

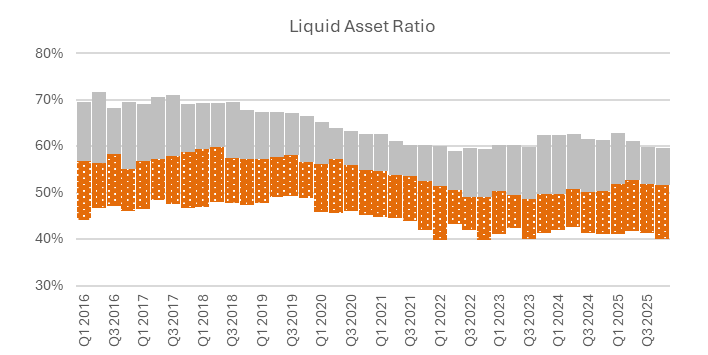

The Liquid Asset Ratio of direct portfolios stipulates in particular illiquidity haircuts by investment class and credit quality.

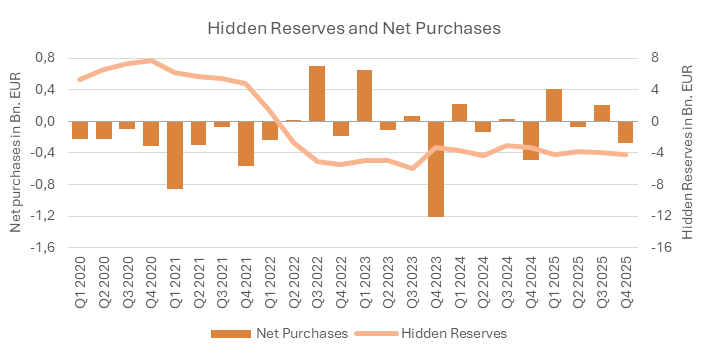

Hidden losses in the balance sheet drawn up in accordance with the Austrian Commercial Code (UGB; Unternehmensgesetzbuch) due to lower market values than book values may impede the sale of assets, as realised losses reduce profits. Due to the purchase of long-term government bonds with higher interest rate sensitivity, changes in interest rates have a greater impact on gains or losses.

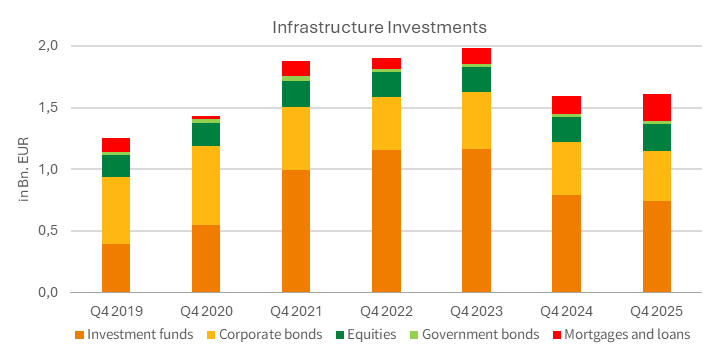

Infrastructure investments are an example of less liquid investments. Special rules exist in the Solvency II framework for own funds requirements for them.