Up until 1990, company old-age provision was primarily based on direct commitments by the employer. Such commitments (frequently referred to as firm or company pensions) were financed by the pensions provisions in the company. In 1990, a new legal framework for company old-age provision was created following the entry into force of the Company Pension Act (BPG) and the Pensionskassen Act (PKG).

- The BPG defined the coverage (under employment law) of benefits and entitlements arising from commitments from company pensions, which are made by the employer to the employee by way of an employment relationship under private law. Such commitments are intended to be covered on the whole by means of two measures. In the event of the employee leaving the undertaking (change of employer) the employee should be protected against losing such pension benefits (vesting). In addition the opportunity of the employer to revoke benefits that have been previously committed should not be excluded, but should instead be materially restricted, since long-term arrangements are frequently made by the employer in good faith about the promised old-age provision and therefore must be all the more protected against such a revocation, since the employee in any case makes advanced payments through their activity for the undertaking.

- The PKG defines how company old-age provision is conducted by Pensionskassen (pension funds).

There are basically two different types of Pensionskasse commitment. In the case of defined contribution commitments (known internationally as defined contribution [DC] schemes) the employer pays contributions to the Pensionskasse that are invested in the capital market. The pension amount therefore depends heavily on the development of the capital markets. The beneficiaries (entitled and recipients) also bear the underwriting risk in addition to the investment risk, since when calculating the pension at the time of the benefit commencing the mortality charts that apply at that time will also apply. In the case of defined benefit commitments (known internationally as defined benefit [DB] schemes) the employer promises in advance to finance a defined pension benefit in accordance with the amount of contributions it makes to the Pensionskasse. The employee bears the investment risk and the underwriting risk. In addition to the two aforementioned types of pensions, there are also various mixed forms, known internationally as “hybrid schemes” (one example of a mixed form would be a defined contribution commitment, which in any case stipulates a minimum occupational invalidity pension, for which the employer shall in the case of such a benefit event occurring under certain circumstances shall be required to make additional contributions up to this minimum amount).

At the forefront of all such variations lies the commitment of a life-long old-age pension. The pension that is required to be offered to survivors (spouse or partner) is generally to be paid out on a life-long basis, although the pension agreement may also stipulate a temporary rule. Orphans’ pensions are usually temporary. Furthermore, in practice nearly all providers offer occupational disability pensions or invalidity pensions. A pre-condition for a pension benefit is a vested claim, which arises once the vested period pursuant to Article 5 para. 1 BPG has been exceeded. In the case of the employment relationship being terminated within the vested period (this shall be a maximum of three years following the employer commencing payment of contributions (cf. Article 5 para. 1 BPG )) the pension claim lapses and the capital hitherto accrued from employer contributions shall benefit the remaining members of the collective. Employee contributions are in any case immediately vested.

Pensionskassen must operate in the legal form of a stock company (Aktiengesellschaft) and have their registered office in Austria. The generally applicable legal conditions that apply to stock companies are to be applied to Pensionskassen, unless stated otherwise in the PKG. It is necessary to differentiate between two types of Pensionskassen:

- Multi-employer Pensionskassen are allowed to manage Pensionskasse commitments of beneficiaries (entitled and recipients) for multiple employers.

- Single-employer Pensionskassen are only authorised to conduct Pensionskasse transactions for beneficiaries (entitled and recipients) of a (single) employer or within a group. They were originally primarily established as the subsidiary of international (groups). On the one hand the purpose is that employees are able to be offered benefits from their “own” Pensionskasse, on the other hand the sponsoring undertakings have a greater influence on investment and the design of the conditions.

The involvement of beneficiaries (entitled and recipients) in the management of the Pensionskasse is a central objective of company pensions and Pensionskasse law. On the whole, beneficiaries (entitled and recipients) have participation rights in the supervisory board of the Pensionskasse, in the advisory committee and in the general meeting.

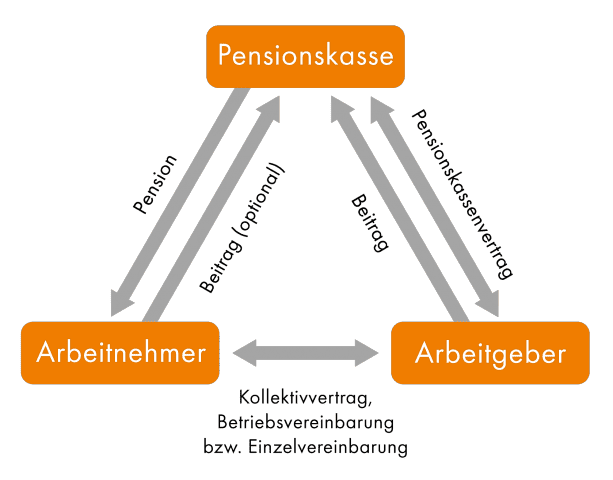

On the basis of a basis under employment law (a works agreement, collective labour agreement or an individual agreement on the basis of a pro forma contract) the employer concludes a Pensionskasse contract with the Pensionskasse pursuant to Article 15 PKG , which implements the Pensionskassen agreement. The latter is a contract for the benefit of third parties, i.e. beneficiaries (entitled and recipients). The termination of the Pensionskasse contract or dissolving it by mutual consent is generally only permissible provided that the transfer of assets to a facility of the ORP listed in Article 17 para. 1 PKG is ensured (for example occupational group insurance or another Pensionskasse).

The cut-off point for termination is 31.12. of each year (balance sheet date of the Pensionskasse), with a notice period of twelve months in the case of termination or a notice period of six months in the case of cancellation by mutual consent.

Pensionskassen conclude Pensionskasse contracts with employers. Such Pensionskassen activities exist in the form of legally binding pension commitments to beneficiaries (entitled) and the provision of pensions to beneficiaries (recipients) and survivors. In this context, Pensionskasse contributions are collected and invested that are paid by the employers (as well as optionally by employees) to the Pensionskasse.

The paid-in contributions are invested by the Pensionskasse in trust and which determine respective pension amount in accordance with the investment result and the technical result.

The assets of the beneficiaries (entitled and recipients) are managed by the Pensionskassen in trust by means of one or more investment and risk sharing groups (IRGs ). The material characteristics of IRGs are:

- The assets of the employees are collectively invested in the IRGs and pursuant to Article 12 para. 1 PKG a risk equalisation conducted (longevity risk, death risk, occupational disability risk).

- The collective (a cornerstone of the Pensionskassen industry) is at the forefront in this case, with there only being a single investment strategy and a single mortality chart within an IRG .

- The assets of the IRG shall only be allowed to be used for paying out pensions.

- Within an IRG the Pensionskasse commitments may be managed by one employer or by several employers.

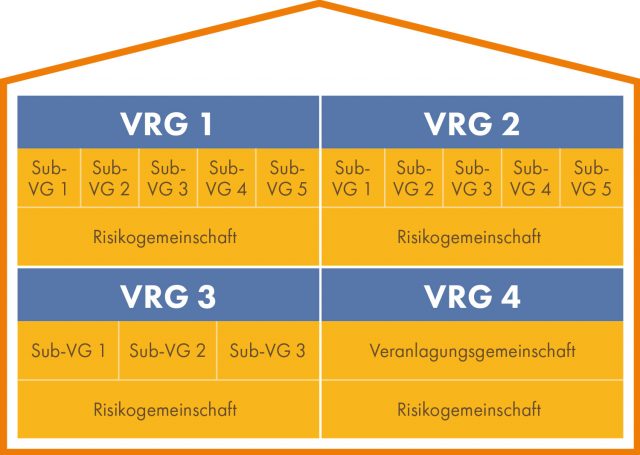

Since 1.1.2013 the option exists pursuant to Article 12 para. 6 PKG to establish sub-Investment Groups (Sub-IGs) in up to three IRGs . Within such an IRG up to five sub-IGs may be established that have different investment strategies.

The following illustration shows as an example a Pensionskasse (PK) with four IRGs , (VRGs ) of which three of the IRGs respectively manage sub-IGs .

A Pensionskasse commitment may also contain individual options. The beneficiary may switch sub-IG as well as IRG up to three times. A pre-condition for doing so is however an arrangement in the Pensionskasse contract.

The IRG assets are protected as special funds in the event of the Pensionskasse’s bankruptcy.

In the collection system of ORPs there are only restricted options available for individual beneficiaries. Overall, however, the system offers the following discretions and options:

- The choice of Pensionskasse rests primarily with the employer, who also concludes the contract with the Pensionskasse. The beneficiary (entitled or recipient) has no direct influence in this case.

- As a rule there is no opportunity for individual beneficiaries to participate in the designing of the Pensionskasse commitment. Usually a beneficiary (entitled or recipient) is included in a Pensionskasse commitment and then receives a monthly pension from the Pensionskasse at a later date.

- Every beneficiary (entitled) is however permitted to make own contributions up to the amount of the employer contributions, in order to increase their pension from the Pensionskasse.

- A further option exists with regard to switching to a security-oriented IRG (see the following section). However, to do so a Pensionskasse must manage such an IRG or alternatively have concluded a corresponding cooperation agreement with another Pensionskasse. Under such a condition, a beneficiary (entitled) may, in the case that they still have an ongoing employment relationship from the age of 55, switch to a security-oriented investment and risk sharing group. No contractual basis is required in this regard.

The technical design of such a an IRG is considerably more cautious than in another IRG , to ensure that it will not be necessary to reckon with either substantial pension adjustments or with large pension reductions. However, the future pension amount will be more moderate. The pension from the Pensionskasse calculated upon retirement in any case determines the future guarantee value, so that this value is never undershot during the benefit phase.

The Pensionskasse pension amount calculated upon retirement does not subsequently remain unchanged, but is adjusted on an annual basis in accordance with investment performance and the technical result. Consequently either increases or reductions are possible, although the amount of the increase or reduction being influenced by both the calculation parameters (the assumed interest rate and the technical surplus) as well as the volatility reserve.

- The assumed interest rate (the maximum permissible interest rate for new Pensionskasse contracts is determined in the FMA’s Regulation on Calculation Parameters for Pensionskassen) is the interest rate that is based on the calculation of the expected benefits or the necessary contributions and therefore constitutes an anticipated return from investment. Where the return from investment for an IRG is below the assumed interest rate and there are therefore otherwise no means available for shoring up the investment result, such as e.g. the volatility reserve, then the pension benefits must be reduced.

- The stipulated technical surplus is a target for the expected result of investment and constitutes a material factor for the calculation of the volatility reserve. An return from investments in the amount of the technical surplus should be achieved for the IRG to fulfil the proposed increases in benefits. If the technical surplus is exceeded in an investment year, the amount exceeding the investment income will be allocated to the volatility reserve. In those years where the technical surplus is not achieved, the shortfall is made up from the volatility reserve.

- The premium reserve constitutes the capital collected for the beneficiaries (entitled and recipients), which is used for calculation pension benefits.

- As a result of fluctuations in the investment performance and the technical result of an IRG of corporate provision funds, there may be fluctuations from one year to the next in the investment performance and therefore pension benefits may also be volatile. The volatility reserve is the equalisation mechanism to avoid such fluctuations or to keep them as low as possible. If the volatility reserve is used up (for example as a result of a continuous prevailing of poor returns of investments), then pension reductions may occur.

In contrast to defined benefit systems, beneficiaries (entitled and recipients) in defined contribution systems participation in the additional performance in good years for investment, but also bear the risk in bad years for investment.

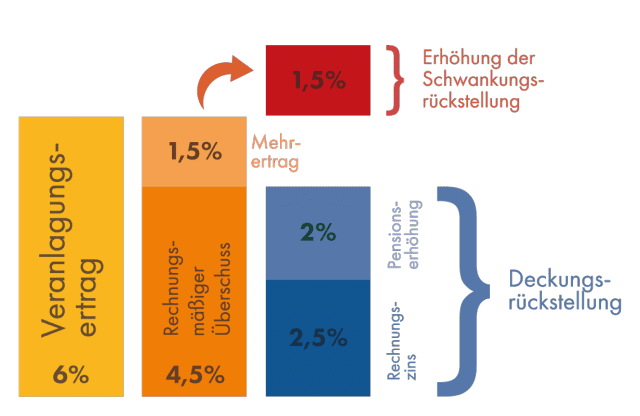

Whether and to what extent there is an increase in pension, depends both on the investment result as well as the technical result.

In any case a high performance from investments does not automatically also mean a commensurately high increase in pension, since the pension increase is ultimately influenced by the assumed interest rate and the technical surplus. Only once the return on investments exceeds the assumed interest rate, is it possible to reckon with a pension increase, since a fictitious return on investment in the amount of the assumed interest rate has already be factored in, i.e. anticipated. This adjustment is in turn limited to the amount of the technical surplus, since returns over and above this amount are allocated to the volatility reserve.

Where the return on investments in a calendar year for an IRG is 6.0%, and the technical surplus is 4.5% and the assumed interest rate 2.5%, then pension payments are increased by 2.0%. The technical surplus that exceeds 1.5% are allocated to the volatility reserve.

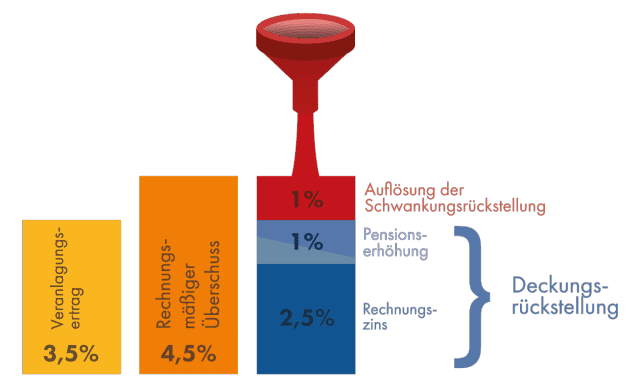

If the return from investments for example is only 3.5%, then pensions may only be increased by 2.0%, when the 1.0% required (the difference between the technical surplus of 4.5% and the return on investments of 3.5%) is able to be withdrawn from the volatility reserve. Should this not be the case, due to, for example, the volatility reserve being empty, then pension increases of only 1.0% can be granted, since this is equal to the difference between the return on investment of 3.5% and the assumed interest rate of 2.5%.

Pensionskassen are required to establish a volatility reserve to balance investment profits and losses as well as technical risks. The reserve thus acts as a buffer to ensure that the investment income expected will be achieved.

Purpose of the volatility reserve

The volatility reserve is a distinct component of the assets of an investment and risk-sharing group that is managed separately from the other assets. It is used to balance fluctuating investment and technical income, thus smoothing out the effect. Beneficiaries (recipients) should be able to count on balanced pension benefits.

Functioning of the volatility reserve

The share of the interest that exceeds the technical surplus is allocated to the volatility reserve. The technical surplus is based on the investment and risk sharing group’s business plan and represents the average expected investment income. The employer may allocate specific contributions to the volatility reserve in order to provide additional security with regard to meeting their pension benefit obligations.

If the technical surplus is exceeded in an investment year, the amount exceeding the investment income will be allocated to the volatility reserve.

In those years where the percentage for the technical surplus is not achieved, the shortfall is withdrawn from the volatility reserve.

The volatility reserve’s target value should be determined by the Pensionskasse’s management board. With regard to the amount of the volatility reserve, the threshold values laid down in the Pensionskassen Act (PKG; Pensionskassengesetz) must be met.

At the end of 2014 the volatility reserve was around 7% of the premium reserve.

Types of volatility reserve

The volatility reserve may be managed:

- collectively – groups of beneficiaries (entitled and recipients) are managed together; or

- Individually – individual beneficiary (entitled or recipient) are managed separately

Except for defined benefit commitments, the PKG prescribes two forms of guarantee for additional occupational pensions.

Pensionskassen are required to give a guarantee for the funds invested unless the provision of this minimum yield guarantee has been excluded. The following sections describe in simplified terms how this guarantee is structured.

Conditions for providing a minimum yield guarantee

The Pensionskasse is generally required to provide the minimum yield guarantee for the funds it invests. However, this minimum yield guarantee can be excluded in the Pensionskasse contract entered into between the Pensionskasse and the employer. In such cases a pension company commitment without minimum yield guarantee exists. The condition for such an arrangement is that a waiver of the minimum yield guarantee has been stipulated in an agreement between the employer and the employees (shop agreement or collective agreement). The consent of the employees (or their representatives) is not necessary with a pension company model based on defined benefits. This is because, in the case of defined benefit commitments, the employer bears the investment risk and the employer contributions are adjusted based on the investment result.

Advantages of excluding the minimum yield guarantee

The notion behind waiving the minimum yield guarantee is to provide for more cost-effective and flexible management options. Under a minimum yield guarantee, any deficit that results is required to be covered from the own funds of the Pensionskasse. In waiving the minimum yield guarantee, the Pensionskasse should achieve potential economies as well as enhanced flexibility, in particular as a result of not using its own funds.

The option of waiving the minimum yield guarantee also corrects competitive disadvantages arising when institutions for occupational retirement provision based in other countries of the European Economic Area are active in Austria. Based on the applicable law of the country of origin, the latter are usually not required to provide any binding yield guarantee.

More than three quarters of all beneficiaries have waived the minimum yield guarantee (as at the end of 2014).

Features of the minimum yield guarantee

The minimum yield guarantee refers to the investment yield of a particular investment and risk sharing group (the technical account balance is not covered by the guarantee). With regard to insurance and investment risks, the beneficiaries (i.e. the individuals entitled to benefits from the Pensionskasse and those already receiving benefits) are managed by one or more investment and risk sharing groups. Employees’ assets are invested jointly in the investment and risk sharing groups so as to balance any risks.

Target value of the guarantee

The minimum yield guarantee is calculated as:

- one half of the average monthly government bond yield weighted by outstanding amounts (UDRB)

- over the last five years

- minus 0.75 percentage points

The UDRB is a weighted average of the yield rates of federal government bonds listed on the Vienna Stock Exchange. As of April 2015, the UDRB replaced the secondary market yield (SMR). The UDRB is based on an extensive database, including both stock exchange and over-the-counter (OTC) transactions.

Reference value of the guarantee

The target value based on the average government bond yield weighted by outstanding amounts is compared with:

- the average annual yield of the investment and risk sharing group

- over the last five years.

If the target value based on the average government bond yield weighted by outstanding amounts is greater than the reference value, a deficit is to be calculated. The pension benefit resulting from annuitising the deficit is to be credited to the beneficiaries (recipients) in the following year, paid out of the Pensionskasse’s own funds.

Once a deficit has been identified, a reference value is to be calculated in the following years in addition to the deficit required to be re-calculated each year. The reference value is calculated in the same way as the deficit, with the calculation period being extended by one year in each of the following years. The deficit and the reference value are compared. The higher of the two values is annuitised and credited to the beneficiaries (recipients) from the own funds of the Pensionskasse in the following year. The credit is independent of the type of pension commitment and the amount cannot be credited with retroactive effect.

Please download the file below for a list of all target and reference target values:

Target Value and Reference Target Value 2025 (Format: pdf, Size: 91,5 KB, Language: English)

Details of calculation procedures are defined in the Minimum Yield Regulation (Mindestertragsverordnung).

The auditing actuary is obliged to verify that the calculation of the deficit and of the reference value as well as their annuitisation comply with the provisions set forth in the Minimum Yield Regulation (Mindestertragsverordnung) and the Pensionskasse’s approved business plan.

To ensure the capability of meeting minimum yield commitments, the Pensionskasse is required to build up a minimum yield reserve. This reserve may be used only to cover benefits arising from minimum yield obligations.

The possibility has existed since 1 January 2013 for beneficiaries who are at least 55 years old, to switch to a security-oriented IRG . Such a switch is only possible at latest upon retirement. The pension which is calculated at the point retirement is guaranteed in the security-oriented IRG . The pension amount may subsequently (depending on the investment performance and the technical result) increase or fall, but however may never fall below the level of the pension at retirement due to the guarantee. In any case this form of guarantee is associated with more cautiously set mortality charts and lower calculation parameters.

Further information: