Views in the discussion about FinTechs vary strongly, including the views held by supervisory authorities on the subject. For what is considered a “developed” term, there is no uniform specification of what one is, with many talking about start-ups and small to medium-sized innovative founders, while others also use the term in relation to established banks, when they launch ground-breaking new business models into the market. To understand what the Austrian Financial Market Authority (FMA) does in the FinTech area – and above all what the FMA can do for you, it is therefore a good idea to know about the FMA’s perspective with regard to FinTech.

FinTech focusses upon information technology-based financial innovations, which

- frequently although not always are developed by companies that do not hold licences,

- typically include interfaces to undertakings that hold licences, and

- may bring sustainable changes to the existing way of functioning of the financial sector.

Companies that are active in the field of such financial market technologies are known as FinTechs. To some extent sub-concepts have already been established, such as “InsurTechs” for the insurance sector. From the latest payment app through to automated customer service systems, the concept of FinTech is a broad one, and encompasses a broad array of different models, which affect many areas of supervision. Many existing financial products or services are discovering new channels via FinTechs and are being conducted by online platforms, apps or new technologies such as “Distributed Ledger”.

FinTechs are frequently companies from the technology sector, whose products and services are connected to or extend other products and services, including those provided by “classical” financial market players. However it is a growing concept, and no national supervisory law regulated FinTechs per se. Both undertakings that hold licences and those that do not may can described as FinTechs, if they bring together new technologies and financial services. In Austria both Austrian and foreign FinTechs are active. Some do not require a licence for their business activities; some are established financial institutions that are currently developing FinTech areas for their existing business models; some FinTechs are currently just starting their activities and have only recently become subject to supervision. In short: FinTechs can cover the whole spectrum of market participants from the classic bank through to the high-tech start-up.

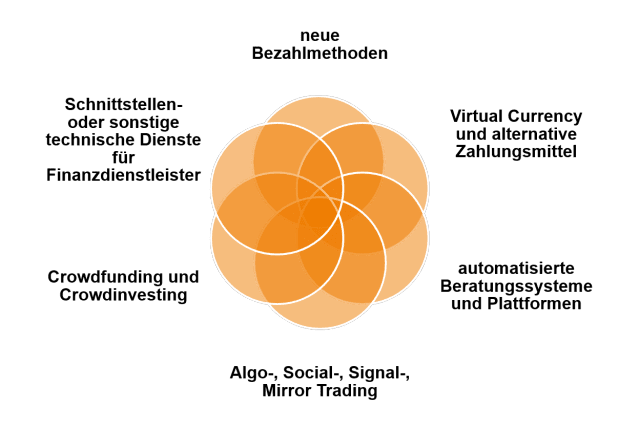

Currently the following business areas are part of the FinTech universe:

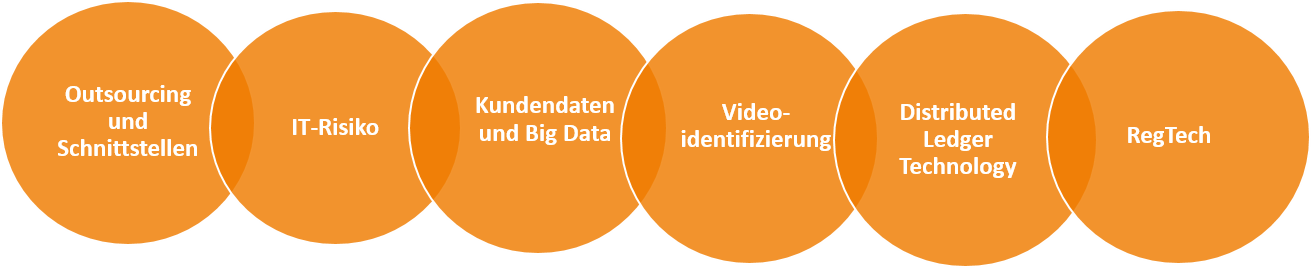

For young tech companies, as well as for classic financial market participants like banks, payment and e-money institutions, insurance companies, investment services, digitalisation has added a particular new perspective to existing issues as well as a whole host of new issues, such as:

FinTech models may be offered by supervised financial market participants such as banks and insurance companies. FinTechs that are not supervised may only provide their services either outside the scope of transactions that require a licence, or in cooperation with market participants that hold the requisite licence. It is frequently not easy to delineate which approach applies, so the Austrian Financial Market Authority (FMA) therefore considers it its task to provide support to FinTechs in clarifying what is possible. If, however, a suspicion arises that transactions are being conducted without the requisite licence being held, then the Austrian Financial Market Authority (FMA) is required to investigate (see Article 22b of the Financial Market Authority Act (FMABG; Finanzmarktaufsichtsgesetz) on unauthorised business operations), and where applicable to prohibit the conducting of the activity as well as to initiate administrative penal proceedings. The Austrian Financial Market Authority (FMA) therefore has several functions: on the one hand it supervises licensed FinTechs as well as licenced entities with FinTech divisions, while also providing clarification about whether a licence is required and whether authorised business operations are potentially being conducted.

You’d like to operate a FinTech or use new technologies? Explain your business model to us in detail and receive information about issues in relation to supervisory law! Use the FinTech Point of Contact to do so.