Legal Basis

Pursuant to Article 23e para. 3 BWG, the FMA may “prescribe by way of a Regulation taking into consideration the relevant Recommendations and Guidelines of the EBA with the consent of the Federal Minister of Finance, that credit institutions and groups of credit institutions maintain on an individual basis, on a consolidated basis or a sub-consolidated basis a capital buffer requirement for the systemic risk buffer consisting of Common Equity Tier 1 capital”. In doing so, the FMA bases the buffer level on a Recommendation by the Financial Market Stability Board (FMSB) as well as an expert opinion (in German only) by the Oesterreichische Nationalbank.

Objective and Composition of the Systemic Risk Buffer

In accordance with Article 23e BWG, the Systemic Risk Buffer (SyRB) is intended to counteract systemic risks that may lead to a disruption with potentially significant detrimental effects on the domestic financial system or domestic real economy. The systemic risk buffer may be set for the banking sector as a whole or parts thereof, in relation to all exposures or a subgroup thereof. The possibility therefore exists to use several systemic risk buffers simultaneously for different exposures. One condition when defining a subset of sectoral exposures is the systemic relevance of the risks that arise from these exposures. For further information, please consult EBA Guidelines EBA/GL/2020/13 (Guidelines on the appropriate subsets of sectoral exposures to which competent or designated authorities may apply a systemic risk buffer in accordance with Article 133(5)(f) of Directive 2013/36/EU).

The buffer rate to be set shall be at least 0.5% with no upper limit. The systemic risk buffer to be met by an individual credit institution is the total of the individual systemic risk buffers. The systemic risk buffer shall not be allowed to cover any risks that are already covers by a Countercyclical Capital Buffer (CCyB) or a Capital Buffer for Systemically Important Institutions and must be appropriate in terms of its effect on the financial systems of other Member States and the European Union.

The objective of the systemic risk buffer is to limit the vulnerability of institutions to systemic risks arising from the financial system or parts thereof by building up additional capital and thereby increasing their risk bearing capacity.

Identified Systemic Risks

Risks from commercial real estate financing (Sectoral Systemic Risk Buffer pursuant to Article 7 para. 2 KP-V 2025)

To address risks arising from commercial real estate financing, a sectoral systemic risk buffer has been required to be held by all institutions since 1 July 2025[1].

The buffer addresses the increased systemic risks arising from the commercial real estate financing portfolio in Austria, from which, according to OeNB analyses, a disruption might arise for the Austrian financial system in a crisis scenario. Such systemic risks are not restricted to individual institutions, but exist for all institutions with commercial real estate financing in their loan portfolio.

A detailed description of the identified systemic risks and the methodology used can be found in the OeNB Financial Stability Report (Systemic risks from commercial real estate lending of Austrian banks, FSR 48, November 2024 as well as in the Explanatory Notes to the recast KP-V 2025 (in German only).

The buffer was prescribed by means of the Capital Buffer Regulation (KP-V 2025; Kapitalpufferverordnung 2025) based on the Recommendation of the Financial Market Stability Board (FMSG/6/2024) of 3 October 2024 after having obtained an OeNB opinion. The currently applicable buffer amounts are set be the amendment to the KP-V 2025 that was published in the Federal Law Gazette on 23 June 2026 (in German only).

We would also like to refer you to the Questions and Answers about the sectoral Systemic Risk Buffer for Commercial Real Estate Financing.

Calibration of Buffer Level

The buffer shall apply to all commercial real estate exposures pursuant to Article 3 KP-V 2025. These are exposures that meet all of the following three criteria.

- they are located in Austria[2],

- they exist towards legal persons or partnerships,

- whose principle activity belongs to one of the following economic activities:

- construction (ÖNACE classification F 41),

- site preparation, construction installation activities, and other construction activities (ÖNACE classification F 43) or

- real estate activities (ÖNACE classification M 68)

although public interest housing associations pursuant to Article 1 in conjunction with Article 34 gem. § 1 iVm § 34 Limited Profit Housing Act (Wohnungsgemeinnützigkeitsgesetz) are excluded.

The buffer amount of 1 % of the total of risk weighted exposure measurements of the commercial real estate exposures of the institution that applied until 1 July 2026, was required to be met both based on the consolidated situation as well as on an individual basis. From 1 July 2026 until 30 June 2027, a buffer amount of 2% applies. From 1 July 2027, a buffer amount of 3.5% applies.

The respective increases of the buffer level to 2% and 3.5% respectively were made based on a Recommendation by the FMSG on 12.12.2025 and an expert opinion by the Oesterreichische Nationalbank (OeNB) – available in German only.

The FMSG’s Recommendation of 12 December 2025 was based on the FMSG’s requesting of a re-evaluation of the systemic risks arising from commercial real estate financing in Austria and the ensuring re-calibration of the buffer level. The background for the ad hoc evaluation performed outside of the regular periodicity of two years for such evaluations was that the entry into force of CRR3 on 1 January 2025 was expected to have a significant impact on the risk weighted exposure measurements of commercial real estate exposures, thereby necessitating a review about the adequacy of the buffer amount as soon as the data for performing one became available. The results were reported to the FMSG at the Board’s 47 meeting, held on 12 December 2025. As a result, the FMSG recommended the FMA to incresed the buffer rates in a two-step process, while at the same time leaving all other parameters for the calculation of the buffer, especially its scope of application, unchanged.

The expert opinion provided by the OeNB in January 2026 continues to show material systemic risks from commercial real estate financing. These systemic risks were derived, as was also the case in the opinion from 2025, by modelling the losses of credit institutions under an adverse scenario (based on the EBA stress test) and the resulting regulatory capital shortfalls. To ensure that there is sufficient available capital in the event of a potentially serious systemic crisis, and to ensure that credit institutions also then meet their regulatory requirements, it is necessary to increase the buffer capital, which can only be achieved with a buffer rate of 3.5%. The 3.5% buffer rate is only sufficient under the assumption that the total risk exposure for the exposures affected by the sSyRB continues to increase in accordance with the prevailing trend since 2020, e.g. as a result of rating downgrades, and taking into consideration all the risk provisioning that has already been made.

The buffer calibration was undertaken under the assumption that the credit institutions that use the standardised approach for credit risk for calculating risk weighted exposure measurements apply the risk weights set out in Article 125 (2) Table 1 CRR for income producing real estate exposures (IPREs) for exposures secured by residential property or set out in Article 126 (2) Table 1 CRR for exposures secured by commercial immovable property, and do not deviate from this course.

The analysis of the impact of the requirements in CRR 3 has shown a low degree of influence on the buffer calibration, and therefore confirmed the appropriate buffer rate of 3.5 % that were already identified in the opinion in 2024.

Effects of the buffer on the economy as a whole

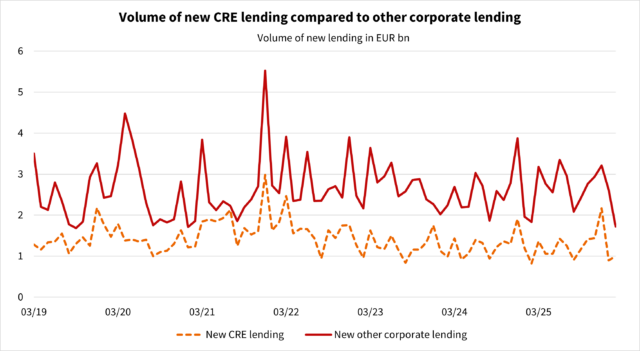

The benefits of the sSyRB in strengthening financial market stability exceeds the costs of the measure to the real economy. At the time of the OeNB’s analysis, the vast majority of Austrian banks hold sufficient free CET1 capital over and above the effective maximum capital requirements when an sSyRB of 3.5 % is applied. The expected economic impacts on the Austrian real economy from increasing the buffer rate to 3.5% are currently assessed as being very low, and no relevant impacts are expected on the granting of credit. OeNB analyses have shown that the introduction of the sSyRB of 1% neither led to an increase in interest rates nor to a fall in new lending volume in affected commercial real estate lending. In the event of short-term adjustment affects being observed at a few banks, then substitution effects are also expected in the credit market due to better capitalised banks. The sSyRB does not cause any impediment for the smooth functioning of the internal market.

Note: CRE loans under sectoral perspectives excluding lending to public interest housing associations. Reporting date of most recent data: 28.02.2026. Only new lending is including. Loans that have been renegotiated have not been considered

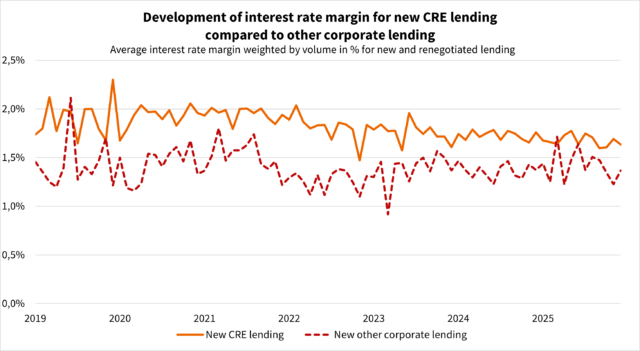

Note: CRE loans under sectoral perspectives excluding lending to public interest housing associations. Reporting date of most recent data: 28.02.2026.

Reciprocal application of the buffer in other Member States

The FMA already requested the ESRB to publish a recommendation on the reciprocal application of measures in all other EEA Member States when the buffer rate was 1%. The ESRB agreed to this request by including the Austrian sSyRB in its Recommendation (ESRB/2015/2) [3] (see Recommendation C, point 1). To date numerous Member States, including Germany, Belgium, Lithuania and Italy, have complied with this recommendation, and have issued corresponding rules for the institutions that fall within their national scope.

In March 2026, the FMA requested the ESRB to issue a recommendation regarding the reciprocal application of the increased buffer rates of 2 % and 3.5% in all Member States in line with its application in Austria. The ESRB also complied with this request, by once more extending its Recommendation (ESRB/2015/2) and published the “Recommendation of the European Systemic Risk Board of 24 April 2026 amending Recommendation ESRB/2015/2 on the assessment of cross-border effects of and voluntary reciprocity for macroprudential policy measures (ESRB/2026/2)” (OJ C/2026/3215).

Approval by the European Commission and ESRB Opinion

As a result of increasing the buffer rate for the sSyRB for individual credit institutions or for groups of credit institutions the sum of the buffer rates for the O-SII buffer, the SyRB and the sectoral SyRB is over 5%, and therefore prior approval was required to be obtained from the European Commission pursuant to Article 23c para. 8 in conjunction with Article 23d para. 6 BWG. The European Commission granted the FMA this approval on 19 June 2026 (see Commission Act C (2026) 4057).

As a result of the increasing the buffer rate for the sSyRB the total capital buffer requirement for the systemic risk buffer for some credit institutions or groups of credit institutions stands between 3% and 5%, on the basis of Article 23e para. 9 in conjunction with para. 6 BWG and Article 133 (11) CRD VI in addition to the aforementioned approval by the European Commission, it is also necessary to obtain opinions from the European Commission and the ESRB about this matter.

The ESRB submitted the corresponding positive Opinion (ESRB/2026/1) to the FMA, which will be subsequently be published by the ESRB. The EBA also published its positive Opinion (EBA/Op/2026/05).

[1] Credit institutions pursuant to Article 1 para. 1 BWG provided they are not excluded under Article 3 BWG or Article 30a para. 6 BWG in conjunction with Article 10 of Regulation (EU) No 575/2013 from having to observe Article 23e BWG (cf. Article 2 KP-V 2025).

[2] The location of an exposure is determined both for the purposes of the calculation of the Countercyclical Capital Buffer as well as the Systemic Risk Buffer in Commission Delegated Regulation (EU) No 1152/2014 supplementing Directive 2013/36/EU of the European Parliament and of the Council with regard to regulatory technical standards on the identification of the geographical location of the relevant credit exposures for calculating institution-specific countercyclical capital buffer rates, OJ L 309, 30.10.2014, p. 5.

[3] The current consolidated version can be found on the ESRB website: https://www.esrb.europa.eu/pub/pdf/recommendations/ESRB_2015_2.en.pdf, and the individual legal act regarding Austria: Recommendation of the European Systemic Risk Board of 4 November 2025 amending Recommendation ESRB/2015/2 on the assessment of cross-border effects of and voluntary reciprocity for macroprudential policy measures (ESRB/2025/10) https://www.esrb.europa.eu/pub/pdf/recommendations/esrb.recommendation251104.en.pdf.

Risks due to systemic vulnerability and systemic concentration risk (Systemic Risk Buffer pursuant to Article 7 para. 3 KP-V 2025)

As the identified systemic risks (at least indirectly) impact the entire banking system, in principle a systemic risk buffer should be prescribed for all banks based on these risks. However, to ensure that proportionality is accounted for, systemic risk buffers are only applied to those banks that are particularly highly exposed to both systemic vulnerability and/or systemic cluster risk areas of risk. In the case of systemic vulnerability there is a differentiation between systemic vulnerability due to interconnectedness or that due to public ownership. In addition, these banks are required to meet a proportionality criterion, for a systemic risk buffer to be applied. If the indicative thresholds for the indicators of the respective risk channel are exceeded, then a systemic risk buffer is to be applied to the bank. The objective is to guarantee the highest possible level of stability in the selection of banks and the calibration of buffer levels, so that volatilities of a non-temporary nature do not lead to buffers being imposed or repealed. The banks’ activities and related trends are monitored, also in consultation with banking supervision at individual bank level. The banks are identified separately on a consolidated and unconsolidated basis.

The identification of banks for the risk of systemic vulnerability on the basis of interconnectedness is based on the following indicators:

- proportion of covered deposits,

- position in the Austrian banking network, and

- as a proportionality criterion the bank’s share of the aggregate total assets of all Austrian banks.

Exposure towards the Austrian banking network is a material indicator for measuring the systemic vulnerability of every individual bank. In the evaluation performed in 2024, for the first time, the indicator was calculated on both a consolidated basis and an unconsolidated basis. This indicator considers both interconnectedness in terms of interbank lending, and the capitalisation of the institutions.

The identification of banks for the risk of systemic vulnerability on the basis of public ownership is based on the following indicators:

- proportion of government ownership of the bank, and

- As a proportionality criterion the share of the aggregate total assets.

“The proportion of government ownership of the bank” is used to select those banks that may contribute to banking crises leading directly to a burden on the public budget due to their ownership structure.

The identification of banks for the systemic cluster risk is based on the following indicators:

- similar business model,

- significance of profitability from the CESEE for the Bank’s total profit for the period, and

- as a proportionality criterion the proportion of the banks’ CESEE exposures compared to Austria’s CESEE exposure as a whole.

Calibration of Buffer Levels

The SyRB and the O-SII buffer have a complementary effect, i.e. they supplement each other. During the transposition of CRD V into Austrian law, this interplay was taken into account accordingly through the additivity of the two buffers. The SyRB buffer levels were reduced accordingly to avoid overlaps with the O-SII buffer (the same risk should not be addressed twice).

Identification of the parts of the banking sector required to maintain a systemic risk buffer

Pursuant to Article 23e para. 3 BWG, the FMA may “set a Common Equity Tier 1 capital (CET1) systemic risk buffer for parts of or the entire banking sector for a subset of or all exposures […], in order to avoid or mitigate systemic risks that are not covered by Regulation (EU) No. 575/2013 or by Articles 23a to 23d, that are manifested in such a way that it might lead to the disruption of the financial system with potentially significant negative impacts on the financial system and the domestic real economy […]”.

The part of the banking sector that is exposed to a relevant extent to the identified systemic risks shall be required to maintain a systemic risk buffer.

The setting of the buffer amounts as well as the identification of the parts of the banking sector and specifically the institutions and groups of institutions impacted by the relevant systemic risks occurred based on an opinion by the Oesterreichische Nationalbank. Detailed descriptions about the methodology applied can be found on the Oesterreichische Nationalbank website.

The systemic risk buffer requirement relates to all the institution’s exposures irrespective of their location.

In its Recommendation dated 12 September 2022, the FMSB has determined that a heightened structural systemic risk exists in Austria. As is also apparent from the OeNB’s opinion, this results from the specific combination of the following factors: low structural profitability, specific ownership structures, high exposure to emerging economies in Europe, the size of the banking sector in relation to GDP, its interconnectedness within the financial economy and with the real economy and the long-term structural spread risk. Based on the FMSB’s Recommendation and the OeNB opinion, it is therefore necessary to activate a structural systemic risk buffer in the following components to address and mitigate systemic risks: (1) systemic vulnerability and (2) systemic cluster risk.

Systemic vulnerability is the risk emanating from the system that affects individual banks, e.g. as a result of market distortions in the wake of a bank’s failure and, in particular, through the risk of a burden on the public budget from banks that are in public ownership. Systemic cluster risk is a risk resulting from substantially similar risk positions across the banking industry and which may lead to disruptions at several credit institutions as a result of this similarity that may have serious negative effects on the financial system and the real economy. However, in accordance with a proportionate application of the capital buffers, only those banks were selected that are particularly exposed to these risks and fulfil a proportionality criterion. The structural capital buffers are only activated for these banks.

Buffer levels are calibrated for the individual systemic risk components. In so doing, structural changes in systemic risks and any overlaps with other regulatory micro- and macroprudential measures are duly accounted for. In its expert opinion on the quantification of the overlap between the systemic risk buffer and the capital buffer for systemically important institutions, the OeNB states that the latter maybe reduced by a maximum of 12.5% in the case of additivity and the former by a maximum of 25%. In calculating the buffer levels, the minimum requirements for own funds and eligible liabilities (MREL) and the resources of the Single Resolution Fund (SRF) that have already been built-up have also been taken into account, because this provides a greater degree of manoeuvrability in cases of resolutions.

As the identified systemic risks manifest themselves at all affected institutions or groups of institutions both at the consolidated and individual institution level, the FMSB recommended the systemic risk buffer should be set on both the consolidated and individual institution level.

According to the OeNB’s opinion, the public ownership of the Landes-Hypothekenbanken hampers their recapitalisation in the event of a crisis (systemic recapitalisation risk). It also states that state guarantees have increased incentive distortions in the past, and continue to exist despite a reduction (expiry of the guarantee obligation). When the Capital Buffer Regulation 2021 (KP-V 2021) was enacted, the reduction of state guarantees was already taken into account where the buffer requirements for the systemic risk buffer for the affected regional mortgage banks were reduced from 1% to 0.5% (cf. Article 8 para. 1 KP-V 2021 compared to Article 7 para. 1 of the Capital Buffer Regulation (KP-V) published in Federal Law Gazette II No. 435/2015 in the version amended by Regulation in Federal Law Gazette II No. 586/2020). As these systemic risks manifest themselves in all affected institutions or groups of institutions both at the consolidated and individual institution level, the FMSB recommended the systemic risk buffer should be set on both the consolidated and individual institution level. The systemic risk buffer is therefore required to also be held by the four identified regional and mortgage banks at the individual institution level. Following the re-evaluation, BAWAG exceeds the relevant criteria for the application of the systemic risk buffer at the individual institution level for the first time. Addiko Bank AG was identified as an additional bank for the application of the systemic risk buffer at the consolidated level due to having a higher systemic cluster risk, while the systemic risk buffer was reduced for UniCredit Bank Austria due to the lower significance of systemic cluster risk at the consolidated level.

The other changes in buffer levels are as a consequence of the implementation of the additivity of systemic risk buffers and capital buffers for systemically important institutions following the amendment to the Austrian Banking Act (BWG), published Federal Law Gazette I No. 98/2021. At that time at the time of the recasting of the KP-V 2021 buffer levels for the capital buffer for systemically important institutions were reduced. The reason for the reduction was that in the midst of an economic environment characterised by high uncertainty due to COVID-19, no buffer increase should occur solely due to a regulatory change. The increases in capital buffer requirements for systemically important institutions that have occurred despite there being no significant change in EBA scores compared to the 2021 evaluation, are therefore due to the fact that the temporary buffer reduction expires when additivity is introduced for the first time. In the final calculation of the buffer levels, the complementary effect of the two capital buffers was however taken into account as part of the overlap analysis.

In addition, the FMSB’s Recommendation is followed to limit the additive requirements from the systemic risk buffer and the capital buffer for systemically important institutions to an additional maximum 0.5 percentage points. Without such a limit, the expiry of the temporary reduction of the buffer in conjunction with the first time introduction of additivity would have led to a stronger increase in effective buffer rates for a few institutions. The reasons for a limit of an additional maximum 0.5 percentage points are both the uncertainties arising from war in Ukraine, increased energy prices and high inflation, as well as the expiry of one-off effects from macro and financial policy assistance during the course of the COVID-19 pandemic, that posed new challenges for banks’ business models (e.g. due to borrowers’ reduced ability to service debts and increased operating costs).

The FMA must review at least once a year whether the capital buffer requirement for the systemically important institutions pursuant to Article 23d para. 8 no. 2 BWG, and the the capital buffer requirement for the systemic risk buffer pursuant to Article 23e para. 5 BWG at least every two years. During the next evaluation of the macroeconomic capital buffers the financial economic and macroeconomic environment including the credit institutions’ and the financial system’s reactions until then are taken into account.

With regard to the impact of the structural capital buffers on the granting of credit it can be determined based on the relevant data that the building-up of capital since the introduction of buffers in July 2016 has not restricted the granting of credit. Since July 2016, the granting of credit by Austrian institutions has continued to develop dynamically, and has always shown positive growth. The impact of the additional capital buffers on growth were explicitly modelled and quantified in the OeNB’s opinion. It was analysed whether an actual capital requirement arises for banks as a result of buffer increases, and what additional costs arise for banks as a result and how they affect key macroeconomic indicators (investments, consumption). The projected negative economic effect of increasing capital buffers is very small, with a maximum reduction in GDP growth of 0.001 percentage points over the next 3 years.

Legal consequences of failure to observe capital buffer requirements

In the event that the credit institution fails to meet the combined capital buffer requirement (see Article 24b BWG), then this results in restrictions on distributions (see Article 24 BWG) and the obligation to prepare a capital conservation plan (see Article 24a BWG).

Further information

The following accompanying explanatory remarks and downloads about amendments to the KP-V 2025 are only available in German.

Kapitalpuffer-Verordnung 2025 (KP-V 2025) (BGBl. II Nr. 112/2025) (Format: pdf, Size: 2,1 MB, Language: German) Begründung zu BGBl. II Nr. 112/2025 (Format: pdf, Size: 606,3 KB, Language: German) Begutachtungsentwurf zur Änderung der Kapitalpuffer-Verordnung 2025 (KP-V 2025) (Format: pdf, Size: 204,3 KB, Language: German) Gutachten zu Begutachtungsentwurf zur Änderung der KP-V 2025 (Veröffentlichungsversion) (Format: pdf, Size: 1,4 MB, Language: German)ESRB Reciprocation of Measures

EBA Opinion about an Austrian macroprudential measure (sectoral Systemic Risk Buffer) - EBA/Op/2026/05 (Format: pdf, Size: 179,3 KB, Language: English)