FMA Climate Stress Tests – Pensionskassen

FMA Climate Stress Tests – Pensionskassen

The Austrian Financial Market Authority (FMA) regularly conducts stress tests to analyse the risks and vulnerabilities of Pensionskassen sector especially with regard to the current economic climate as well as for assessing the risk capacity of the individual Pensionskasse. For this purpose, the FMA also examines the impacts of future climate policy, the advent of low-carbon technologies, the economy’s level of adaptation or the occurrence of extreme events.

In addition, various climate stress tests are conducted on the assets side to analyse the risks and vulnerabilities of Austrian Pensionskassen arising from environmental and inflation risks. Under the current scenarios, shocks were assumed that were in line with the European Commission’s Fit for 55 package (Green Deal). The European Green Deal’s objective is for the EU to achieve climate neutrality by 2050. The European Commission has accepted a range of proposals, to design the EU’s climate, energy, transport and fiscal policy in such a way that nett greenhouse gas emissions can be reduced by at least 55% compared to the levels for 1990 (Fit for 55 package).

The financial system’s resilience while implementing the Fit for 55 package is intended to be evaluated in a scenario analysis, and findings reached about the financial system’s ability to support the transition to a lower carbon economy even under stress conditions. The FMA has applied the accompanying European Systemic Risk Board (ESRB) stress test scenarios.

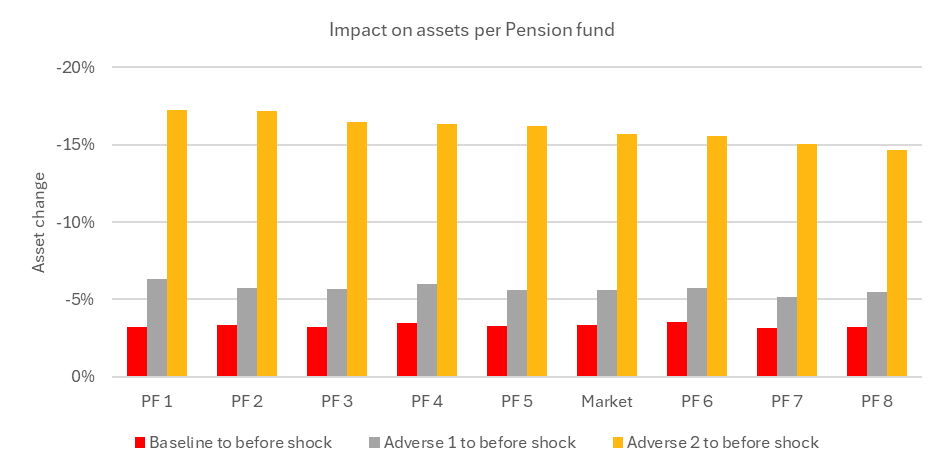

- The baseline scenario reflects a smooth, timely, and widely expected green transition, in which governments implement the political measures of the Fit for 55 package (reduction of emissions by 55% compared with 1990 values) as intended. In this way considerable reductions in fossil fuel emissions levels will be achieved, that are in line with the EU’s objectives for 2030 and the objectives of the Paris Agreement. These developments occur in an economic environment that correspond to the baseline scenario for the European Banking Authority (EBA)’s EU-wide stress test from 2023 (2023-2025) and the subsequent Nationally Determined Contributions (NDC) scenario of the Network for Greening the Financial System (NGFS) (2026-2030).

- The first negative scenario contains a sudden negative revaluation of the transitional risks and is characterised by a sudden shock in confidence. The shock consists of a sudden reversal of the perception of climate-related risks, is not traced back to the transposition of the Fit for 55 package and is reflected by a sell-off of assets designated as “brown”. The shock, which represents a flight from brown assets to non-brown assets, manifests itself in the form of higher financing costs for brown companies, and applies for the period between 2026-2030.

- The second negative scenario takes into account an intensification of climate-related shocks considered in the first negative scenario, and the globally deteriorating macroeconomic conditions, in line with the adverse scenario of the EU-wide EBA stress test and applies to the years 2023-2025. The intensified stress factors combined with the flight from brown assets, which applies for 2026-2030, require far-reaching government interventions for promoting the green transition, which leads to a surge in public sector borrowing and leads to concerns being raised about debt sustainability.

See the pages (in German only) on FMA-Informationsveranstaltungen or Berichte zur Lage der österreichischen Pensionskassen for further details.