National Stress Tests

National Stress Tests – Pension Companies

The Austrian Financial Market Authority (FMA) regularly conducts stress tests to analyse the risks and vulnerabilities of the pension company sector especially with regard to the current economic climate as well as for assessing the risk capacity of the individual pension companies. In this case the effects of a low interest environment that prevails for a long period of time, a sharp increase in interest rates (combined with a broadening of the credit spread) as well as the effects of variously market events are tested and various liability-side shocks simulated.

Instruments for analysing the Risks and Vulnerability of the Pension Companies Sector:

- Sensitivity analyses (usually) relate to a single risk factor and measure the potential reaction of a performance or risk indicator depending on how it changes. This is based on standardised changes in risk factors, the magnitude of which is not necessarily required to relate to economic conditions (in terms of being probable, improbable, historical, etc.)

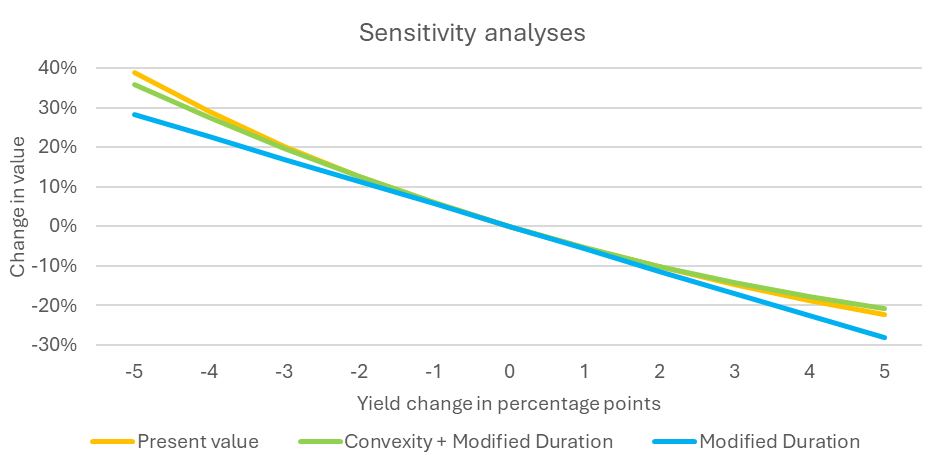

In this way, the FMA regularly analyses the sensitivities of Austrian pension companies’ bond portfolios on the asset side of the balance sheet. The accompanying calculations are conducted using an individual cashflow breakdown, including recalculating the present value as well as by using approximations. The latter is conducted on the basis of the modified duration – both with and without convexity.

- Scenario analyses as a rule are based on changes in (one or more) risk factors that follow an economic narrative, i.e. where their magnitude is estimated with regard to probability or plausibility.

- Stress tests are scenario analyses that are based on extreme yet nonetheless plausible changes (shocks) in risk factors.

- In the case of Reverse Stress Tests the change is selected in such a way that the indicators in question achieve a certain target value.