Solvency Risks

Solvency Risks – Insurance

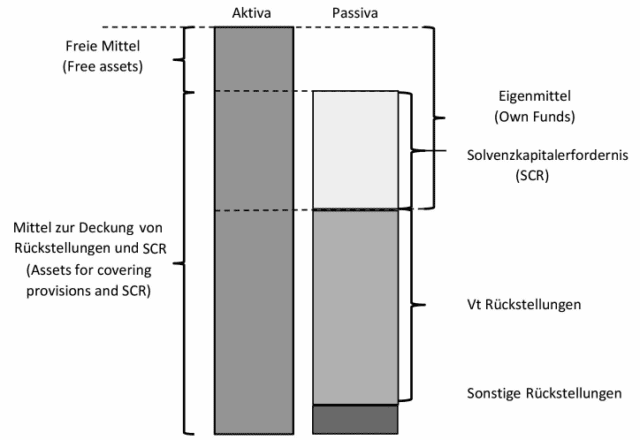

Solvency Balance Sheet

In addition to the balance sheet drawn up in accordance with the Austrian Commercial Code (UGB; Unternehmensgesetzbuch) /Insurance Supervision Act 2016 (VAG) (in accordance with Chapter Seven of the Insurance Supervision Act 2016 (VAG; Versicherungsaufsichtsgesetz 2016)) undertakings that are subject to the Solvency II Regime are additionally required to draw up a solvency balance sheet (in accordance with Chapter 8 of the VAG). Special validation rules apply to them. The solvency balance sheet serves as the basis for calculating the Solvency Capital Requirement, for which the corresponding amount of own funds must be held.

Technical provisions

(Re)insurance undertakings ((R)IUs) are required to form technical provisions to ensure that they are able to meet their payments in relation to their insurance obligations. In addition to insurance benefits, such provisions generally include coverage contributions for covering the costs of concluding and administering insurance contracts. Under Solvency II, no prudent assumptions are required to be met when determining the technical provisions, which is the case for the Austrian Commercial Code (UGB; Unternehmensgesetzbuch). Prudent should be understood in this instance as acting diligently. The principle of market-consistent valuation is also applied to technical provisions. As a result, pricing of obligations constitutes the fundamental idea behind the solvency balance sheet. The value of the technical provisions corresponds to the current amount that (R)IUs would have to pay in the event that they were to transfer their insurance and reinsurance commitments to another (R)IU without delay. Under Solvency II, the technical provisions are reflected in the balance sheet at their current market price. However, it remains a challenge to implement this principle, as no (liquid) market exists for trading in technical provisions. Valuation therefore requires assistance from actuarial models (“Mark-to-Model”). Technical provisions are split into two parts in the solvency balance sheet:

- Best Estimate: The Best Estimate consists of cash flows related to the provision of insurance obligations. These include premiums and payments to insurance policyholders as well as the operating costs of insurance business. The expected value of future cash flows should be calculated using the corresponding risk-free interest rate curve in order to determine the Best Estimate (BE).

- Risk margin: Together with the BE, the risk margin makes up the technical provision. Under Solvency II risk margin is calculated using a Cost of Capital Approach (CoC-Approach). The idea behind this is that the risk margin reflects the capital costs that the IU incurs for holding the required solvency capital that is needed to cover its insurance obligations during their term.

Solvency Capital Requirement

Since every (R)IU is exposed to a multitude of different risks that could threaten its healthy economic performance and therefore also the claims of insured persons, numerous instruments under supervisory law exist to counter such risks. However, they are only able to reduce existing risks and hazards, but never to fully eliminate them. As an additional safety element, (R)IUs are therefore continuously required to hold a legally prescribed minimum own funds requirement (Solvency Capital Requirement (SCR) and Minimum Capital Requirement (MCR)). Under Solvency II, the standard formula for calculating the SCR doesn’t only apply insurance risks related to life, health and non-life insurance, but also market risk, credit risk and operational risk. In addition to the prescribed standardised model for calculating the Solvency II Solvency Capital Requirement, the (R)IU is also free to development a (partial) internal model, to use it to calculate their Solvency Capital Requirement once it has been approved by the supervisory authority. In addition to the risk-based Solvency Capital Requirement (SCR), the factor-based Minimum Capital Requirement (MCR) constitutes a lower threshold for required own funds, which if breached would trigger an ultimate intervention by the supervisory authority.

The Solvency Capital Requirement (SCR) is a target value for the regulatory solvency capital requirement determined by the Value-at-Risk (VaR) and which is required to be covered by suitable levels of own funds. The Solvency Capital Requirement should enable the (R)IU to absorb unforeseen losses on the following year. The SCR is added to the liabilities side of the solvency balance sheet as a risk capital requirement in addition to the provisions. The SCR is calculated on the basis of the going concern principle so that all quantifiable risks are taken into account to which an (R)IU is exposed. It covers both ongoing business activities as well as new business that is expected during the following twelve months. Regarding ongoing business activities it only covers unexpected losses. It corresponds to the Value-at-Risk of the basic own funds of an (R)IU with a 99.5 % confidence level over the period of one year. Expressed in other terms, the SCR reflects the maximum annual loss that is to be expected on average once every 200 years.

The Solvency Capital Requirement may be calculated using the following approaches (Article 175 para. 1 VAG):

Standard formula

The standard formula is calibrated in such a way that the target criterion of a Value-at-Risk (VaR) of 99.5 % is achieved over a one-year period. The material quantifiable risks that most (R)IUs are exposed to should be captured using the standard formula for the SCR. By its nature and characteristics, a standard formula is a standardised calculation method that is therefore not explicitly tailored to a specific undertaking’s individual risk profile. The SCR standard formula follows a modular approach, under which the total risk to which an (R)IU is exposed is subdivided into risk modules and, in some risk modules, also into sub-modules. A capital requirement is determined for each risk module (or sub-module).The capital requirement is aggregated at risk module or sub-module level using predefined correlation matrices to obtain the capital requirement for the total risk.

Internes Modell

Internal models for calculating the SCR are required to be reviewed and certified by the supervisory authority. Certification only occurs if the internal model takes the (R)IUs risk profile into account better than the standardised model, and provided that statistical standards, and calibration, validation and documentation standards are observed. They may be used in the form of full or partial models. Partial models are only applied to a few risk categories or business areas of the (R)IU.