Investment Rules

Investment Rules in relation to Stress Tests – Insurance

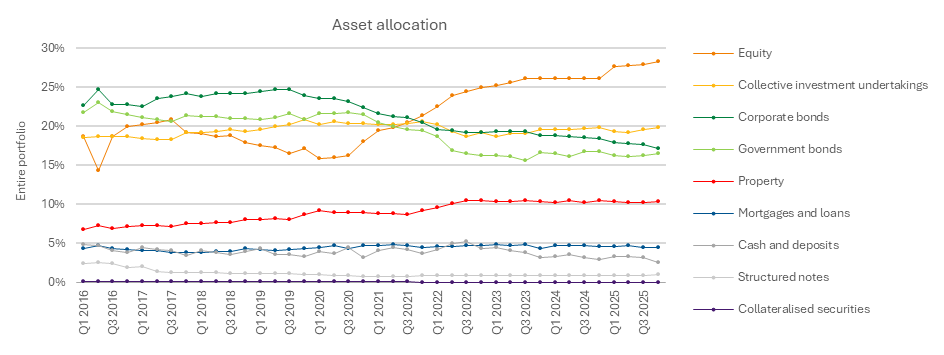

If insurance undertakings change how they invest, then their risk and financial market stability may also change. Investments influence insurance undertakings’ own funds and their volatility via the balance sheets drawn up based on market values under Solvency II. Investment also changes the solvency capital requirement and the ratios. The Austrian Financial Market Authority (FMA) also monitors investment behaviour in conjunction with the regulations set out in the Insurance Undertakings Investment Regulation (VU-KAV 2015; Versicherungsunternehmen-Kapitalanlageverordnung). The FMA develops methodological approaches and improves the data basis.

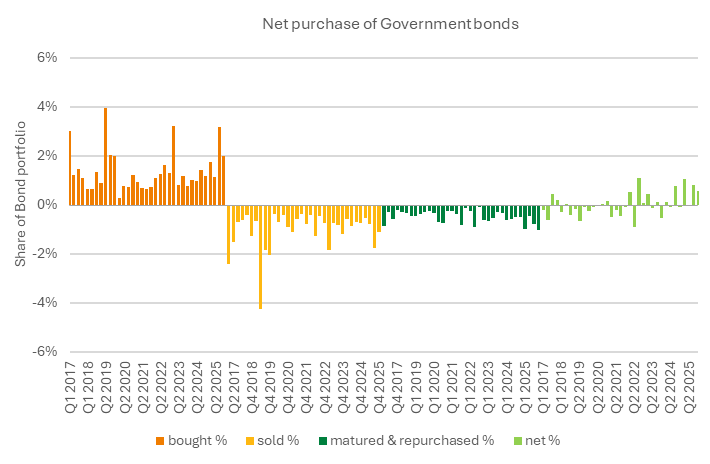

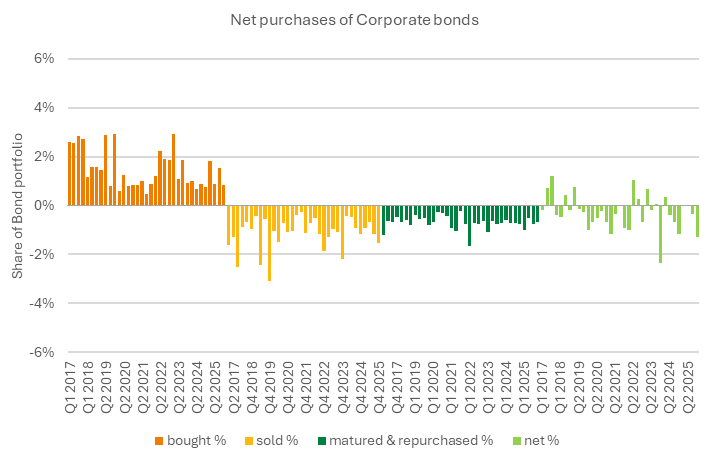

Traditionally, insurance undertakings are net purchasers of bonds. This applies in Austria for government bonds, which are purchased primarily by life insurance undertakings with long maturities. Corporate bonds, particularly those in the financial sector, are being sold on a net basis, as maturing and sold bonds are being replaced by fewer purchases.

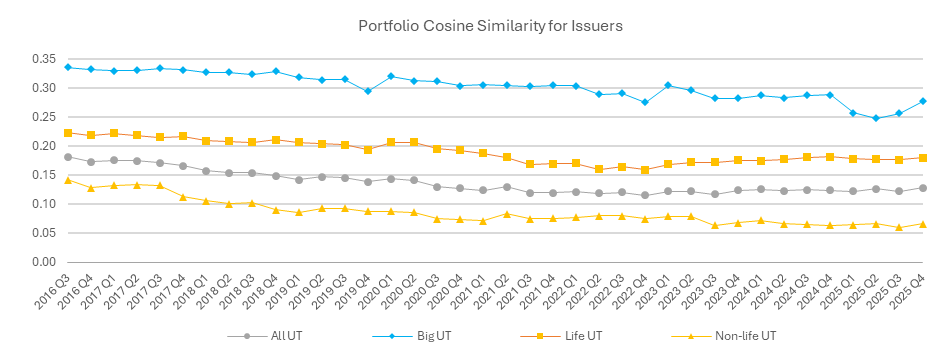

The cosine similarity index measures the risk of contagion due to portfolio overlaps for example in relation to issuers. Portfolio Cosine Similarity is the normalised scalar products of the vectors of issuer weightings of two insurance undertakings respectively. Recently the level of similarity of portfolios has started to increase again.