Investment Rules

Investment Rules in relation to Stress Tests – Pension Companies

The prudent person principle for the investment of capital of pension companies (PKs) has applied in Austria since Directive 2003/41/EC on the activities and supervision of institutions for occupational retirement provision (IORP I) was transposed. The prevailing principle in Anglo-American countries that is also applied by other countries with economically significant private pension systems, largely stipulates a standard of conduct rather than quantitative thresholds for individual asset classes.

Under the Pensionskassen Act, this general principle of prudence is based on the following facets:

- assets are to be invested in the best interests of beneficiaries (entitled and recipients);

- in the event of a potential conflict of interest, investment decisions shall be made exclusively in the interest of beneficiaries (entitled and recipients);

- assets are to be invested in such a way that ensures the security, quality, liquidity and profitability of an asset allocated to an investment and risk-sharing group (IRG) as a whole;

- assets are to be invested by type and duration in a manner that corresponds to the expected future pension provision benefits;

- securities must primarily be listed or traded on a regulated market;

- derivatives shall only be allowed to be purchased for hedging purposes or for facilitating efficient portfolio management;

- assets are to be appropriately diversified, and a concentration of risks duly avoided; purchasing assets from one and the same issuer or issuers belonging to the same group of undertakings, shall not be allowed to lead to an excessive concentration of risks;

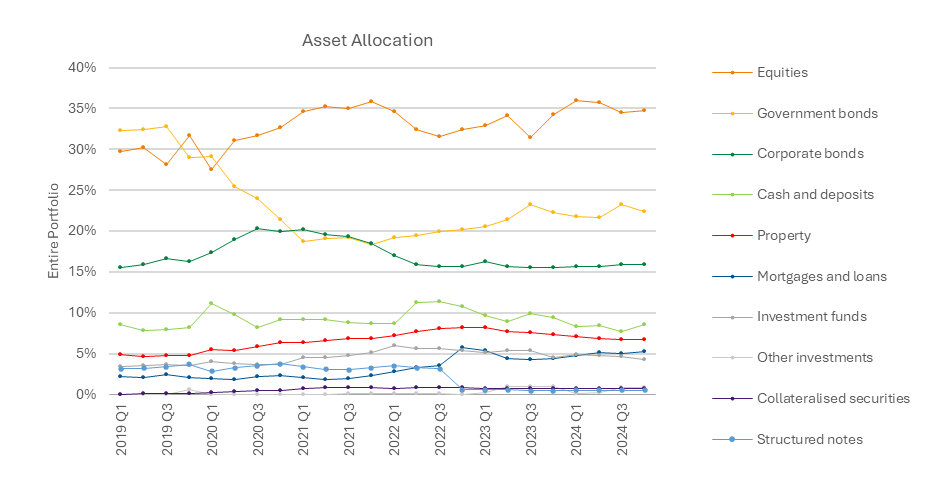

Pension companies have reduced their asset allocation in bonds in recent years. Single employee pension companies in particular have changed their allocation in bonds in favour of equities or other assets.

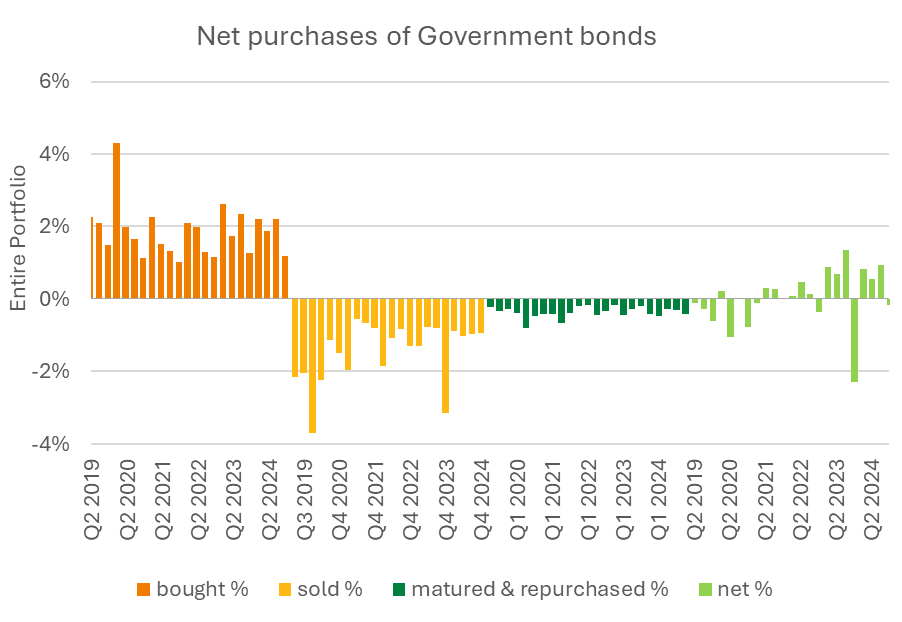

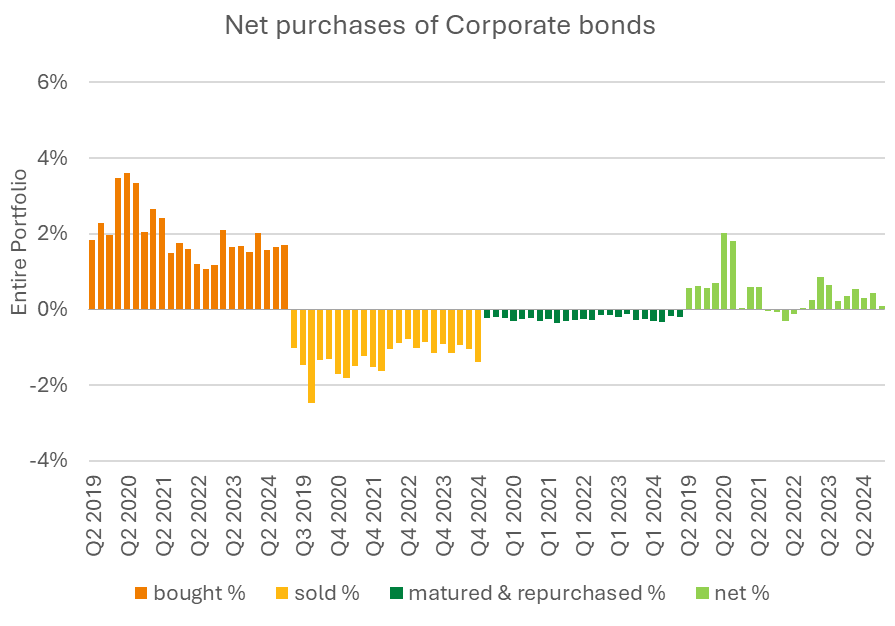

During the final quarter of 2023, when a downturn in economic growth and the Purchasing Managers’ Index pointed to a recession in the Euro area, the funds of pension companies sold government bonds. This was compensated for again in 2024 by purchases that even exceeded the redeemed volume. At same time, and also following the increase in interest rates, multi-employer pension companies in particular have been net purchasers of corporate bonds since Q3 2022. Their investment behaviour in relation to bonds differs from those of insurance undertakings, with insurance undertakings having reduced their holdings in corporate bonds since 2023.