Liquidity

Liquidity in relation to Stress Tests – Pension Companies

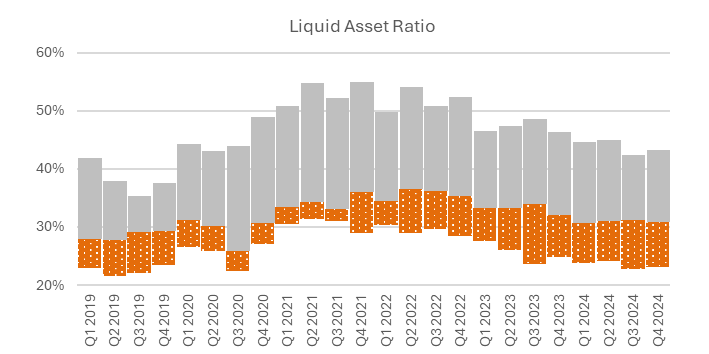

While banks perform a maturity transformation, in the case of pension companies liquidity risk plays a subsidiary role as a general rule. In conjunction with financial market stability risks, the Austrian Financial Market Authority (FMA) investigates the liquid asset ratio, i.e. the proportion of liquidity-weighted assets to total assets.

Illiquidity haircuts, in particular by asset class and credit quality are stipulated for the proportion of liquid assets. The 30.2% median of the Liquid Asset Ratio in Q4 2024 is below the European median for institutions for occupational retirement provision, which stands at 52.2%, and is also lower than the median for insurance undertakings of 51.4%. This is confirmed by pension companies having a higher allocation to funds of over-the-counter assets.