During the course of the revision of EMIR, the European Commission drew up a proposal to overhaul the system of supervision of central counterparties (CCPs). The proposal stipulates a differentiation between non-systemically important (Tier 1) and systemically important (Tier 2) CCPs in relation to CCPs whose registered office is outside the EU-27 (third country CCPs). The existing equivalence regime is only intended to continue to apply for non-systemically important Tier 1 CCPs. In contrast, it is stipulated that the material EU supervision requirements under EMIR shall apply directly for systemically important Tier 2 CCPs. Furthermore, they should also be directly supervised by ESMA and the respective issuing central in the EU, in whose currency clearing takes place (for the Euro this is the European Central Bank (ECB)). ESMA and the ECB have also been conferred more rights and powers within the scope of supervision of EU CCPs. ESMA and the ECB therefore gain voting rights in the supervisory colleges for EU CCPs and national supervisory authorities must obtain an opinion from ESMA and the ECB in relation to certain supervisory decisions. The European Commission’s proposal was implemented in Regulation (EU) 2019/2099 (EMIR 2.2), and has been in force since 1 January 2020.

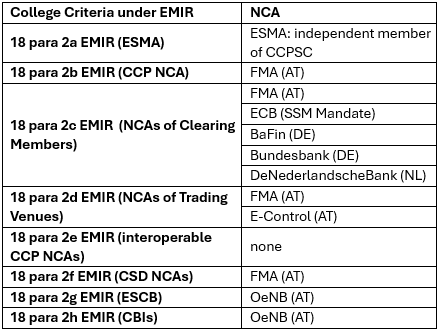

The competent national supervisory authorities in conjunction with an international supervisory college, consisting of representatives of the supervisory authorities of the most important/largest members and market infrastructures of the respective CCP, are responsible for the supervision of EU CCPs. These are in addition to the ESMA: the supervisory authorities of the largest clearing members, the trading venues served, the linked central securities depositories (CSDs), as well as certain central banks, ECB and the SSM (details are defined in Article 18 EMIR). Pursuant to Article 18 (2) EMIR 2.2, every national competent authority is required to publish the composition of the respective college of its website.

Pursuant to Article 2 para. 1 of the Central Counterparties Enforcement Act (ZGVG; Zentrale Gegenparteien-Vollzugsgesetz), the FMA is the competent authority for CCP Austria Abwicklungsstelle für Börsegeschäfte GmbH (CCP.A). CCP.A is responsible for the clearing of spot market transactions on the Vienna Stock Exchange (Wiener Börse) and of all day-ahead electricity spot market transactions executed on the energy exchange platform of EXAA Abwicklungsstelle für Energieprodukte AG. It has held the respective EMIR licence since 01 August 2014. The composition of the supervisory college for CCP.A is as follows (last update March 2026):

More information

Law

European Market Infrastructure Regulation, EMIR

Regulation (EU) 2019/2099 (EMIR 2.2)

Central Counterparties and Trade Repositories Act (ZGVG, in German only)