The Markets in Crypto Assets in Regulation (MiCAR) fully entered into force on 30 December 2024. As a result, the mandatory preparation of a white paper in accordance with Title II of MiCAR is of key significance.

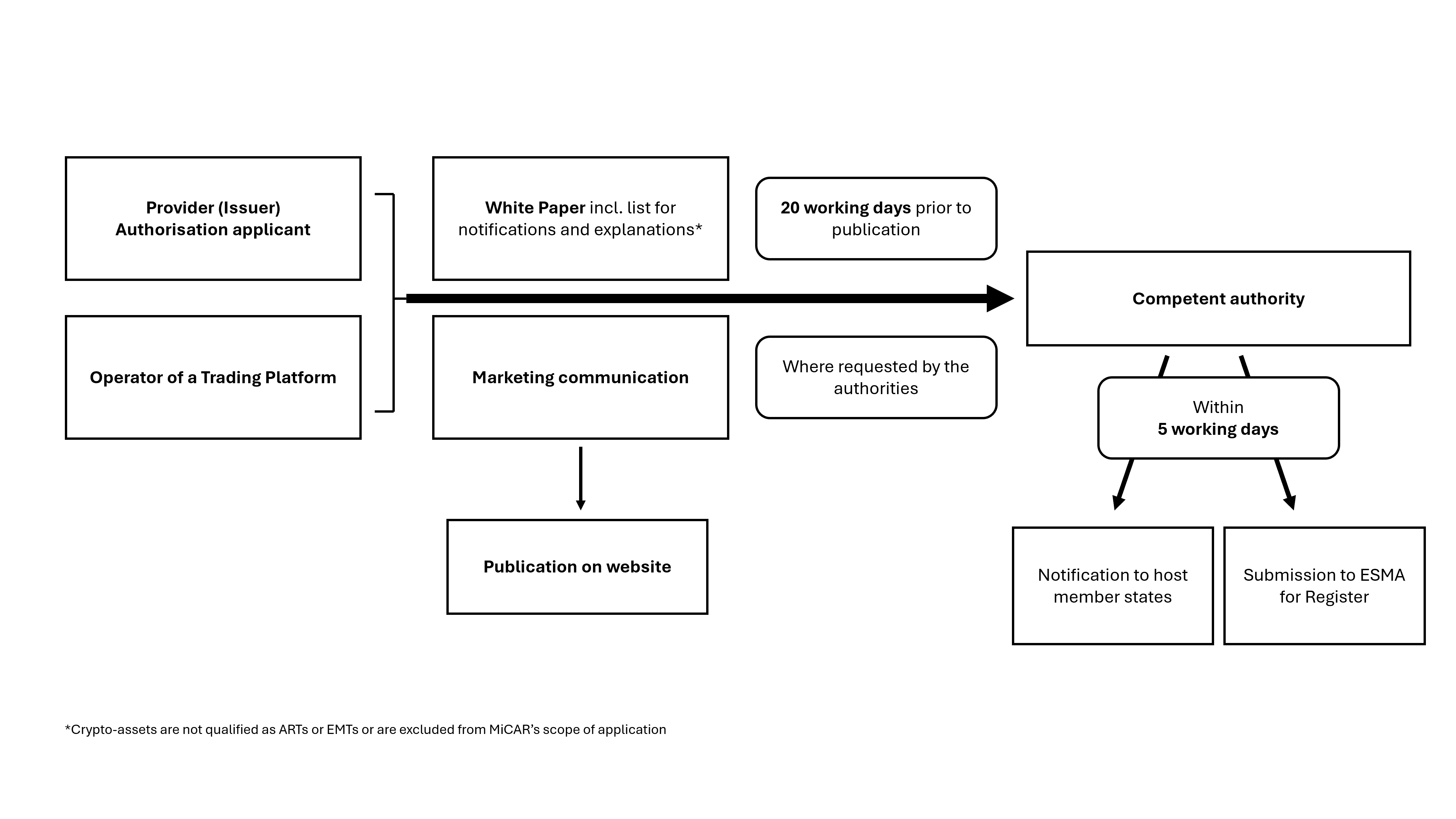

Providers of crypto-assets other than asset-referenced tokens (ARTs) or e-money tokens (EMTs), as well as persons applying for the admission to trading of such crypto-assets, are required to prepare a white paper in accordance with Title II of MiCAR at least 20 days prior to publication and to notify it to the Austrian Financial Market Authority (FMA) as the competent authority for Austria, provided no exceptions apply. The white paper, among other things, much present and describe the material features of the crypto-asset, rights and obligations and the associated risks.

Regarding the structure and content of the white paper, we refer to the sample text contained in Table 2 of Implementing Regulation (EU) 2024/2984 as a template. For information about the impact on the climate, see the sample text contained in Delegated Regulation (EU) 2025/422 as a template. Article 2 defines the requirement for the format of the crypto-asset white paper, which must be drawn up using the Inline XBRL 1.1 specifications of the eXtensible Business Reporting Language (XBRL) marked up in XHTML format. ESMA provides the respective instructions and taxonomy including templates.

When submitting the white paper an explanation pursuant to Article 8 (4) MiCAR must also be submitted. The offeror must state in this explanation why the crypto-asset described in the white paper is not excluded from the scope of MiCAR pursuant to Article 2 (4) MiCAR, and why it is not an e-money token (EMT) or an asset-referenced token (ART). The Joint Guidelines on templates for explanations and opinions, and the standardised test for crypto-assets, under Article 97(1) of Regulation (EU) 2023/1114 (Format: pdf, Size: 357,9 KB, Language: English) published by ESMA contain a template (Annex A) about the explanation as well as more precise rules about how scrutiny has to occur.

In contrast to capital market prospectuses, the FMA does not issue an approval in the form of an administrative decision for the white paper for other crypto-assets. Once a 20-day period has expired, the white paper may be published, and the crypto-assets publicly offered or approval applied for.

Firstly, it should also be noted that the provisions in Title II of MiCAR do not apply for offers that had already ended before 30.12.2024 (Article 143(1) MiCAR). A white paper pursuant to Articles 4 et seq. MiCAR is required to be prepared for crypto-assets that are (still) publicly offered after that date.

Electronic Submission

Please use the following address for all white paper submissions in accordance with Title II MiCAR: https://webhost.fma.gv.at/epass2

The white paper under Title II of MiCAR must be submitted electronically using the FMA’s Secure Electronic Prospectus Portal (SEPP) – the electronic prospectus approval portal that already exists for capital market prospectuses.

To obtain access to the electronic submission portal, the submitting party needs to register, which can also be done in advance. Once the account has been approved, an entry mask (from 30.12.2024) can be reached via a button for submitting Title II – white papers. Then the white paper, the necessary explanations under Article 8 (4) MiCAR, as well as the confirmation of payment of fees must be uploaded as documents.

Instructions about registration and submission of white papers pursuant to Title II MiCAR can be found here:

The submitter of prospectuses can only see those documents in the electronic submission portal which they either submitted themselves or for which they were listed as the representative for the original submitter. For every first-time submission, it is necessary to state the function in which the white paper is being submitted. In the case of lawyers admitted to practise in Austria, it is generally sufficient to refer to having been granted power of attorney. If someone else is acting as the submitter of the white paper (e.g. employees of the issuer, advisers etc.) then a power of attorney must be submitted to the FMA. A pro forma power of attorney can be found here:

Sample Power of Attorney - White Paper (Format: docx, Size: 35,8 KB, Language: English)

Obligation to pay fees

The filing of the white paper triggers the obligation to pay a fee under the FMA Regulation on Fees (FMA-GebV; FMA-Gebührenverordnung). The fee for the filing of the white paper for other crypto-assets other than asset-referenced tokens or e-money tokens is EUR 750 in accordance with fee item III.O.12 of the FMA-GebV. The fee for filing a modified white paper is EUR 500 in accordance with fee item III.O.13 of the FMA-GebV.

The fee must be paid at the same time as filing the white paper into the account held at the Oesterreichische Nationalbank (IBAN AT55 0010 0000 0011 5525, BIC NABAATWW). payee “Finanzmarktaufsichtsbehörde gemäß Finanzmarktaufsichtsgesetz, BGBl. I Nr. 97/2001 – Subkonto für Gebühreneinnahmen”. The purpose of the payment must be in the form “Issuer Token Abbreviation Whitepaper”.

Contact

Austrian Financial Market Authority (FMA)

Division III/4

Otto-Wagner-Platz 5

1090 Vienna

[email protected]

Questions and Answers

The FAQs below contain an overview about the most importance questions about Title II of MiCAR. The list of questions can not however be considered to be exhaustive.

MiCAR defines itself as what is known as a secondary regime. This means that the Regulation does not apply for crypto-assets falling under the exemption set out in Article 2 (4) MiCAR. The exemptions in particular include financial instruments as well as deposits that fall under their own supervisory regimes (e.g. the Securities Supervision Act (WAG; Wertpapieraufsichtsgesetz), the Banking Act (BWG; Bankwesengesetz) or the Deposit Guarantee and Investor Compensation Act (ESAEG; Einlagensicherungs- und Anlegerentschädigungsgesetz))

MiCAR, as a directly applicable EU Regulation, enjoys precedence of application over national law. In order to achieve a harmonisation of the rules that apply for offerors within the European Union, no information requirements or rules may be imposed over and above those set out in MiCAR upon offerors of other crypto-assets as defined in Title II MiCAR.

Where a crypto-asset falls within the scope of application of MiCAR, then the KMG 2019 as well as the AltFG also do not apply even where the corresponding criteria are met.

For crypto-assets within the scope of application of MiCAR then a MiCAR white paper is required to be prepared and published, but no investment prospectus or AltFG information document.

MiCAR chooses a technology-specific term for crypto-assets, and defines them as a digital representation of a value or of a right that are able to be transferred and stored electronically using distributed ledger technology or similar technology. (Article 3 (1) point 5 MiCAR).

Other crypto-assets under Title II MiCAR are defined by means of a negative delineation of Asset-Referenced Tokens (ARTs) and E-Money Tokens (EMT) as well as financial instruments (“Security Tokens”) and therefore forms a collective term that is not defined more closely in the form of a catch-all activity that presupposes the characteristic of being a crypto-asset.

In any case, it includes “utility tokens” meaning a type of crypto-asset that is only intended to provide access to a good or a service that is to be supplied in the future by an issuer.

It also covers NFTs (“Non-Fungible Tokens”), that are issued as partial units, especially when issued in large series or collections.

Under Article 8 (1) MiCAR, white papers of “other crypto-assets” under Title II of MiCAR must be submitted to the competent authority of the home member state. The home Member State is determined in accordance with Article 3(1) (33) MiCAR.

The following possibilities exist in this provision:

a. the provider has its registered office in the European Union

In this case the white paper must be submitted to the competent authority of the country of its registered office.

If the offeror’s registered office is e.g. In Germany, then Austria would not be the home Member State, and the FMA would therefore not be the competent authority under MiCAR.

In this case, if a submission is planned under Article 8 MiCAR to be made to the FMA, then the provider must have its registered office in Austria.

b. the provider does not have a registered office in the European Union, but does have one or more branches in the European Union

It the provider’s registered office is in a third country, but they have one or more branches in the EU, then the provider may choose the home Member State from the Member States in which it has a branch. If it has a branch in Austria, then the white paper pursuant to Article 8 MiCAR may be submitted to the FMA as the competent authority.

c. the provider has its registered office in a third country and does not have any branches in the European Union

If the provider’s registered office is in a third country, and it does not have any branches in the EU, then the home Member State – and therefore also Austria – may be freely chosen.

The only condition in this case, would be that it is (also) offered publicly in this chosen home Member State.

In contrast to ARTs or EMTs, no authorisation procedure is necessary for issuing other crypto-assets. A white paper in accordance with Title II of MiCAR is required to be drawn up at least 20 days prior to publication and submitted to the FMA as the competent authority in Austria for a public offering or admission to a trading platform of such crypto-assets. The white paper does not need to be approved: once 20 days have passed, by publishing the white paper the public offering of the crypto-assets may take place or authorisation may be applied for.

For other crypto-assets there are also regulations regarding marketing communications (Article 7 MiCAR), affording a right of withdrawal for retail holders (Article 13 MiCAR), conduct obligations of the issuers or offerors (Article 14 MiCAR) as well as relating to the issuer’s or the offeror’s liability for the content of the white paper (Article 15 MiCAR).

Whenever significant new factors, material mistakes or material inaccuracies are found in the published white paper that are capable of affecting the assessment of the crypto-assets, modifications are required to be published and filed with the FMA (Article 12 MiCAR).

If the crypto-asset offering is addressed to less than 150 persons per Member State, or exclusively for qualified investors, or where the total consideration of the crypto-asset issued does not exceed EUR 1 million, then the crypto-asset is excluded from the obligation to draw up a white paper (Article 4 (2) MiCAR).

Furthermore, crypto-assets that are offered for free are also excluded. An offering shall not be considered as free, where personal data must be provided in exchange (Article 4 (3) lit. a MiCAR).

An exception also exists for crypto-assets, that are issued as a reward during the course of mining/minting (Article 4 (3) lit. b MiCAR).

Utility tokens that provide an access to goods or services that already exist or are in operation are also excluded (Article 4 (3) lit. c MiCAR).

The crypto-assets are also excluded in the event that they can only be exchanged in a limited network of merchants with contractual agreements with the offeror (Article 4 (3) lit. d MiCAR).

Unlike in the case of capital market prospectuses, the FMA does not grant an approval in the form of an administrative decision or any other written confirmations for white papers for other crypto-assets.

Firstly, it should also be noted that the provisions in Title II of MiCAR do not apply for offers that had already ended before 30.12.2024 (Article 143(1) MiCAR). A white paper pursuant to Articles 4 et seq. MiCAR is required to be prepared for crypto-assets that are (still) publicly offered after that date.

If a crypto-asset was already admitted to trading prior to 30.12.2024, then the provisions in Articles 7 and 9 MiCAR apply for all subsequent marketing communications.

In addition, operators of trading platforms shall ensure by 31.12.2027 that the respective white paper pursuant to Articles 4 et seq. MiCAR have been prepared, published and modified where applicable for all crypto-assets falling in the scope of application of MiCAR (Article 143(2) MiCAR).

Retail holders who purchase other crypto-assets have the possibility to withdraw from their agreement to purchase of other crypto-assets within a period of 14 calendar days without incurring any fees or costs and without being required to give reasons. The withdrawal period shall begin from the date of the agreement of the retail holders to purchase those crypto-assets (Article 13 (1) MiCAR). In addition, the retail holders is explicitly to be informed about this right in the white paper (Article 13 (3) MiCAR).

All payments including fees are to be repaid to the retail holder within 14 days. The repayment shall be made using the same means of payment as was used for the original transaction, unless explicitly agreed otherwise as provided that the retail holder does not incur any costs (Article 13 (2) MiCAR).

The right of withdrawal shall not apply if the crypto-asset was already admitted to trading prior to its purchase (Article 13 (4) MiCAR).

Yes, issuers, offerors and the operators of a trading platform assume liability for information that is not complete, fair or clear in a white paper (Article 15 (1) MiCAR).

This liability shall not be allowed to be contractually excluded or limited (Article 15 (2) MiCAR).