The following section contains information on specific aspects of the catalogue of services of crypto-asset service providers. Parties interested in an authorisation as well as undertakings that are already operationally active are recommended to take these aspects into account accordingly when planning and structuring their business models. Persons and undertakings active in this field that did not previously fall within the scope of supervision are recommended to analyse their business processes regarding the applicability of the new legal provisions, and to adjust them as applicable.

The following remarks have a purely informational character and do not constitute a separate legal basis. Rights and obligations extending beyond the provisions under law may not be derived from them.

Advice in relation to crypto-assets

The Providing advice on a commercial basis in relation to crypto-assets pursuant to Article 3(24) MiCAR constitutes a service requiring an authorisation. Ultimately, this activity may only be conducted from 30.12.2024 by authorised providers as defined in Article 59 MiCAR (undertakings for which the transitional provision pursuant to Article 143(3) MiCAR in conjunction with Article 23 of the Mica Regulation Enforcement Act (MiCA-VVG; MiCA-Verordnungs-Vollzugsgesetz) applies may continue to conduct these activities until the end of 2025 at the latest).

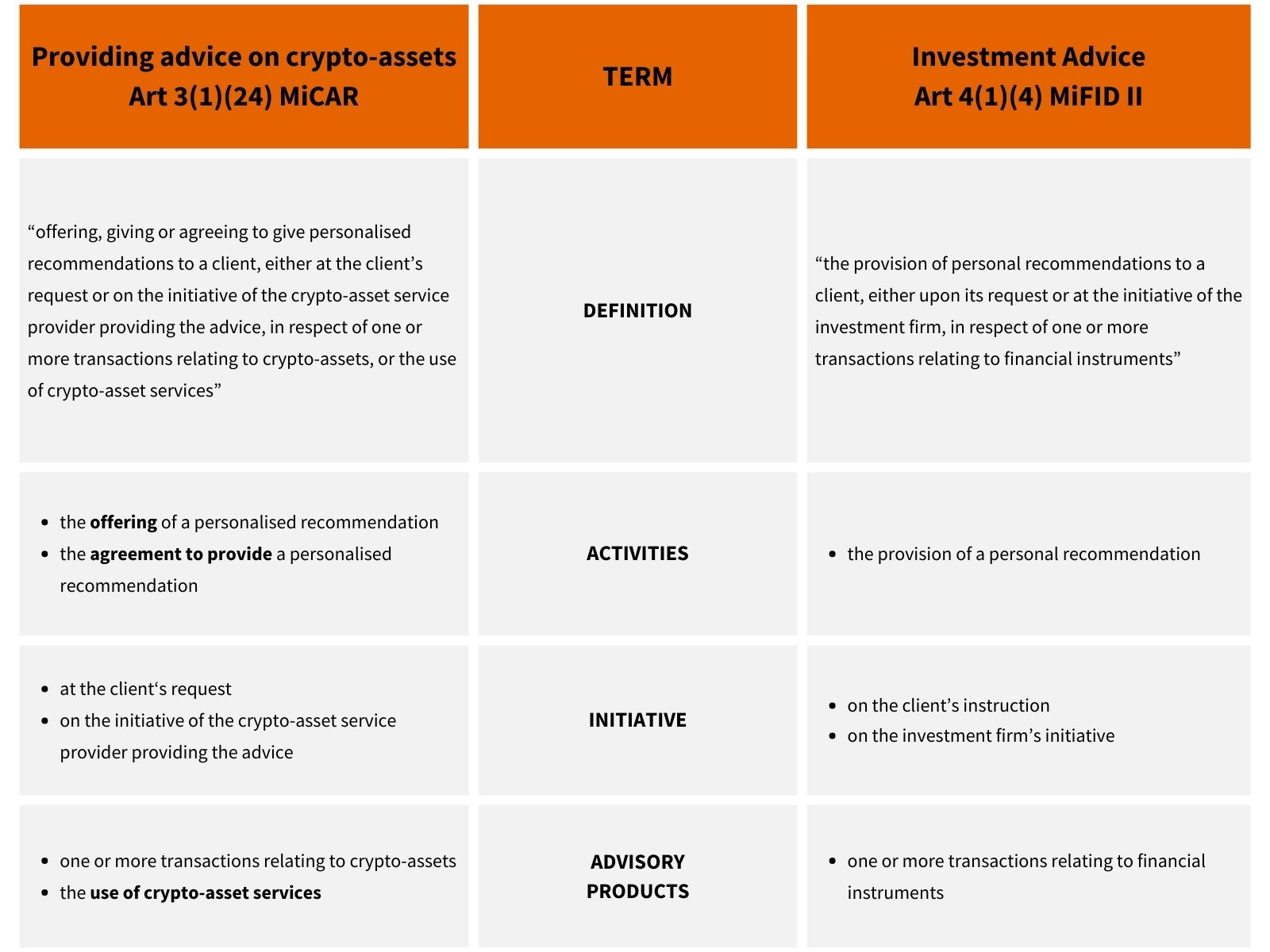

Advice in relation to crypto-assets under the Markets in Crypt-Assets Regulation (MiCAR) in its fundamental aspects corresponds to the established concept of investment advice in relation to financial instruments within the scope of the EU’s Markets in Financial Instruments Directive (MiFID II). However, its definition is broader, and therefore also covers additional activities extending over and beyond purely advisory services in relation to the asset in question. In this light, the following differences exist:

Scope of advisory services in relation to crypto-assets

The relevant activities constituting advisory activities under MiCAR comprise:

- the offering of a personalised recommendation to clients;

- the agreement to provide a personalised recommendation to clients;

- the provision of a personalised recommendation to clients;

Therefore even the fixed initiation of such a future advisory relationship is covered by the authorisation obligation set out in Article 59 MiCAR and therefore may only be conducted by authorised crypto-asset service providers.

The difference between a recommendation as opposed to mere information is characterised by the adviser’s implicit or explicit proposition. In this sense a proposition is to be understood as an activity, statement or other means of signalling by the adviser to the (potential) investor, to motivate them to conduct a transaction or not to conduct one, and/or to use a service, or at least to influence the (potential) investor in this way. Negative recommendations may also constitute investment advice, such as in advising against investing in certain crypto-assets or services. Recommendations to “hold on” to investments, i.e. a recommendation not to make any change to a portfolio, are also included.

For a recommendation to be considered to be personalised, it must be addressed to a person in their capacity as an investor or a potential investor or as the agent of an investor or potential investor. This recommendation must be presented as being suitable for the person in question or must been based on a review about the personal circumstances of that person, and must be aimed at prompting them to take a certain course of action or not to do so.

It already suffices, if from the perspective of the typical investor the impression might be aroused that the recommendation given is based on a review of the affected person’s personal circumstances, and by doing so appears to be personalised. An actual review of the person’s circumstances by the adviser is not required to exists, where the impression of personalised advice exists.

The dissemination of non-personalised information such as a marketing communication, general financial analysis and comparable items and information that is exclusively disseminated for the public and which therefore is made to a general group of addressees.

Whether a personalised recommendation exists in a specific case, therefore depends on the individual circumstances in relation to the case in hand.

The following advisory products may constitute advice in relation to crypto-assets under MiCAR:

- Advice in relation to crypto-assets under MiCAR

- Advice in relation to the use of crypto-asset services under MiCAR

Advice in relation to crypto-assets under MiCAR therefore covers the provision of individual recommendations to a client in relation to transactions with crypto-assets as well as the use of crypto-asset services.

This covers on the one hand the providing of information, valuations and market estimates in relation to crypto-assets that are subject to regulation – i.e. advice regarding crypto-assets – as well as expert advice regarding the composition or expansion of a specific client portfolio by conducting transactions – and therefore the structuring of the client’s assets.

In light of the broad definition of advisory services under MiCAR in relation to the use of crypto-asset services covered by regulation, for example, the following activities may be covered:

- Recommendation of service providers: Recommendation of specific crypto-asset service providers (e.g. operators of trading platforms, wallet providers, custody service providers), whose services offered seem particularly suitable for specific purposes or requirements for the client. These may be based on aspects like security, fee structure, user-friendliness and regulatory compliance as well as factors like liquidity, trading volume, range of offering or special functions or products that the provider offers.

- Optimisation/Adaptation of service usage: Recommendations to use existing crypto-asset services, for example a specific custody solution (hot vs cold wallets, multi-signature wallets, or similar) of a specific product solution (e.g. earn and staking products) based on individual client requirements.

- Integration in existing systems: Recommendations for financial integration of crypto-asset services the client’s existing financial or management systems, such as for undertakings that wish to include crypto-assets in their balance sheet, or to accept them as payment instruments. Activities that can be allocated to the fields of legal or tax advice or auditing are excluded. Purely technical services such as the establishment of blockchain-based solutions for specific corporate processes are also excluded.

- Advice in relation to risk: Advice for identifying and minimising clients’ individual risks in conjunction with using specific crypto-asset services, including compliance with regulatory requirements and security standards associated with their use. This does not include, for example, activities that can be allocated to the fields of legal or tax advice or auditing are or (outsourced) activities of organisational key functions of a CASP, such as those of a compliance officer.

- Technical Assistance and Training: Provision of training or technical support for using specific crypto-asset services, such as how a client sets up or uses a wallet or an account on a trading platform, provided that doing so is based on a client’s individual requirements. In-house or outsourced functions of a regulated service provider like customer support are not covered by this.

Article 81 MiCAR defines the relevant rules within MiCAR about the requirements and obligations regarding advice in relation to crypto-assets. However, it should be noted that the European Securities and Markets Authority (ESMA) will also publish specific Guidelines in accordance with Article 81 (15) MiCAR that will be material for implementing certain regulatory requirements.

Furthermore, under Article 9 MiCA-VVG the FMA shall be required to publish the required knowledge and skills that natural persons providing advice on behalf of an authorised crypto-asset service provider or for using crypto-assets or that give out relevant information. In this light, the information available here is therefore still subject to change.

MiCAR does not contain any regime in relation to the involvement of independent sub-intermediaries within the scope of the provision of crypto-asset services requiring an authorisation. The outsourcing of such an activity to independent third parties, who are active on behalf of and on account of an authorised provider, and who should therefore conduct advisory services as defined above is only possible where they, as defined in Article 59 MiCAR, themselves are authorised to provide the crypto-asset service in question.