General

Platform operators that are authorised pursuant to Article 12 of the ECSP Regulation (see the page on Information for Applicants for Authorisations), are supervised by the FMA on an ongoing basis and are allowed, depending on their authorisation to provide one, several or all of the following services:

- Receiving and transmitting of orders in relation to transferable securities. This corresponds to the service that is already regulated in MiFID II (Annex I, Section A No. 1) and the Securities Supervision Act 2018 WAG 2018) (Article 1 no. 3 lit. a)) and which previously required a licence under WAG 2018, or an activity as a securities intermediary or tied agent for a licensed investment services provider.

- Placing of transferable securities without a firm commitment basis This corresponds to the service that is already regulated in MiFID II (Annex I, Section A No. 7) and WAG 2018 (Article 1 no. 3 lit. g) and previously required a licence as a credit institution under the BWG.

- Loan mediation: this platform operator service was also previously permissible under the Trade Code (GeWO 1994), or by holding a licence as a credit institution. Until the introduction of the specific exception in the ECSPR, the taking of money from the public through a platform by project owners would have been classified as deposit-taking business under the BWG (Article 1 (3) (a) ECSPR). Generally, the creditor would also have been conducting lending business under the BWG. Under the ECSPR users are now able to grant loans via a platform and take moneys over one without having to hold the relevant banking licence.

- Individual management of loan portfolios: The platform operator receives an individual mandate from the investor to allocate a defined amount on the crowdfunding platform to loan projects. In that case, the platform operators is also responsible for a Key Investment Information Sheet (KIIS).

In this instance the threshold of EUR 5 million per project owner per year must be observed. For more information see the point “Thresholds”.

The services listed in the ECSPR relate to the primary market i.e. the initial issuance or distribution of participations in projects by issuers through the ECSP platform to the investor. In contrast ECSP service providers are not allowed to operate multilateral trading platforms. There are only allow to operate “bulletin boards” in the area of secondary market trading through which buyers and sellers can find one another.

On platforms under the ECSPR, only the following instruments are allowed to be offered:

transferable securities pursuant to Article 2 (1) (m) ECSPR (the definition corresponds to Article 1 no. 5 WAG 2018, irrespective of their technical form. It therefore equally covers traditional physical securities in the same manner as securities for which no physical certificate is issued, especially also

- tokenised securities. See also: What constitutes a security as defined in Regulation (EU) 2017/1129 or WAG 2018? and Tokenisation and Crowdfunding.

- investments in the form of loans, that investors grant to project owners through the platform pursuant to Article 2 (1) (b) ECSPR.

The following investment forms or instruments in particular are not permitted on ECSP platforms:

- units in alternative investment funds under the Alternative Investment Fund Managers Act (AIFMG): projects that are offered on crowdfunding platforms and for the financing of which securities are issued must as a rule be operationally active. See also “Projects without an operative activity”

- Investments under the KMG 2019: in particular, the frequently occurring financing arrangements on the Austrian crowdfunding market by means of qualified subordinated loans are not allowed to be distributed using platforms under the ECSPR. For the intermediation of such investments a platform in accordance with the Alternative Financing Act (AltFG; Alternativfinanzierungsgesetz) is necessary. For further details see Austrian Crowdfunding Platforms under the AltFG.

- Furthermore, pursuant to Article 8 ECSPR, a strict prohibition applies on the participation of the crowdfunding service provider in projects or project owners, that are offered of its platform.

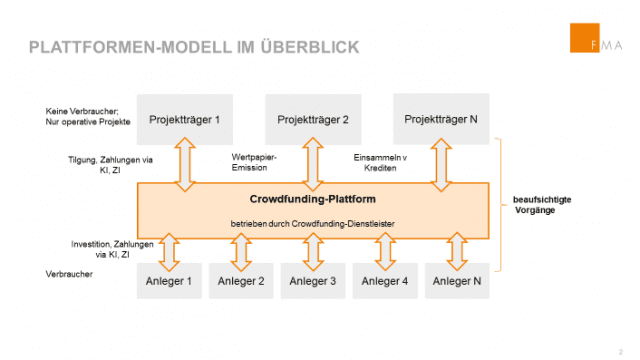

An overview of the players

An overview of the players involved in a crowdfunding service is as follows:

It is particular important for investors to be aware that the crowd investments through platforms under the ECSPR are neither subject to deposit protection, nor to protection provided by an investor compensation scheme. This is a considerable difference compared to traditional securities transactions through investment firms and credit institutions. The Key Investment Information Sheet (KIIS) must also inform that this is the case.

If the crowdfunding platform wishes to broker other instruments such as participations by limited partners, participation rights or qualified subordinated loans, then the offering does not fall within the scope of the ECSPR, but that of the AltFG – see below. Offerings outside of the scope of the ECSPR are not possible in a straightforward manner, without taking into account any regulation that applies in the other country. Projects by consumers do not fall within the regulatory framework (typically in the case of P2P lending models; such models would be addresses strictly under national law, see further below. Crowdfunding without a platform also continues to remain a purely national issue (outside the scope of the ECSPR); i.e. without a publicly accessible Internet information system that has a single operator. This may for example relate to funding arrangements that crowdfunded, which are conducted directyl between a municipality and its inhabitants.

Key Investment Information Sheet (KIIS)

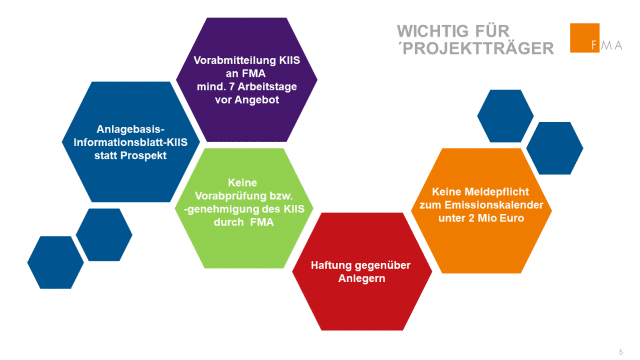

The Key Investment Information Sheet (KIIS) is of particular meaning for investor protection on crowdfunding platforms under the ECSPR. The project owner is required to draw one up for every crowdfunding offering (securities or loans). It should take into account the specificities of project owners as well as the risks of investing, and concentrates on significant information about the project owners, the rights and fees for investors as well as the type of instruments offered. The key investment information sheet replaces the prospectus that would otherwise be necessary for securities under the Prospectus Regulation and is set out in Article 23 ECSPR, as well as in further detail in Regulatory Technical Standards (RTS) that have not yet entered into force. See Annex VIII of the Final Report about the RTS which contains the provisional text in English.

Where a packaged investment product exists, the key investment information sheet also replaces the PRIIP key information document in accordance with Regulation (EU) No. 1286/2014.

An important point to remember: the key investment information sheet is not separately checked and approved by the FMA, as is otherwise the case for a capital market prospectus for securities. The Key Investment Information Sheet is generally drawn up by the project owner, who is liable towards the investors for the information contained therein. The platform is required to make the KIIS available.

Article 27 ECSPR contains specific requirements regarding the content, layout and distribution of marketing communications in relation to crowdfunding platforms under the Regulation. They must be clearly recognisable as marketing communications, must provide a balanced view of the offers on the platform and must be fair, clear, and not misleading. In addition, if being distributed in Austria, they must also be available in German. To assist internationally active platform operators the European Securities and Markets Authority (ESMA) has made an overview about the national rules for marketing communications in the individual EU Member States on its website.

In accordance with Article 25 ECSPR, crowdfunding service providers are allowed to establish secondary market platforms, on which investors may sell on their crowd investments. Such platforms do not however function as exchanges (no matching!) or as brokers (no proprietary trading by the operator!), but instead only function as “bulletin boards”, that buyers and sellers use to find one another.

Under the Regulation, a platform operator shall only be allowed to receive payments on its own account and to transmit them onwards provided that it is also authorised in accordance with the Payment Services Act 2018 (ZaDiG 2018). The platform operator shall also only be allowed to hold payment accounts for customers where it holds an authorisation as a credit institution under the Austrian Banking Act (BWG; Bankwesengesetz). Similarly, a platform operator shall only be allowed to take over the custody of investors’ securities, where it is authorised accordingly to do so.

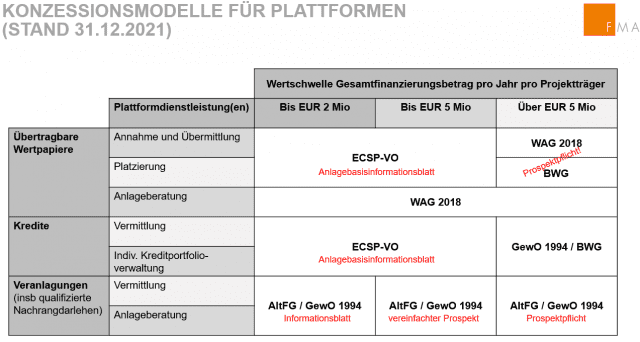

Thresholds, prospectuses and (Key Investment) Information Sheets

The above graphic shows roughly which supervisory regime and in particular which key investor information documents (KIIDs) are required for an offering in each case. Public offerings of securities and investments in Austria are generally subject to the obligation to publish a capital market prospectus. The obligation to publish a prospectus for securities is harmonised throughout Europe in the Prospectus Regulation. Securities prospectuses are checked by the FMA are authorise the issuer for distribution throughout Europe.

The obligation to publish a prospectus for investments (e.g. Participations by limited partners, participation rights) only acknowledges Austrian law in the Capital Market Act 2019 (KMG 2019; Kapitalmarktgesetz 2019). Investment prospectuses must be filed at the OeKB’s notification office prior to publication and are checked by a suitable prospectus auditor (as a rule an external auditor). The FMA must be notified in advance of how the investment prospectus will be published, and where it will be available. Investment prospectuses may only be used for distribution in Austria.

The simplified prospectuses in accordance with Annex D to the KMG 2019 are also only set out in Austrian law, which may by used for issuances of investments and securities of up to EUR 5 mn per year and which only apply in Austria.

In the scope of application of the AltFG and the ECSPR, the capital market prospectus is replaced by shorter information documents that are intended to improve investor protection primarily by means of the clear overview that they contain and their understandability: these are the information document under the AltFG and the Key Investment Information Sheet under the ECSPR. It is necessary to note that issuers with several issuances both within and outside the scope of the ECSPR are required to include their crowdfunding offerings in the threshold amounts for the Prospectus Regulation (Article 5 para. 3 and Article 12 para. 3 KMG), so that when these thresholds are exceeded an obligation to publish a prospectus exists.

For the first time, the ECSPR enables Europe-wide and prospectus-free distribution of securities via a platform.

The Key Investment Information Sheet (KIIS) which is not required to be pre-approved by the FMA is the successor to a capital market prospectus approved by the FMA. Where an issuer/project owner exclusively uses platforms under the ECSPR during the course of a year for issuance and exclusively for the issuance of securities, then they offer up to EUR 5 million in securities without the need for a prospectus publicly and throughout Europe, or less where they also where it also receives loans through such platforms. It is a different case where within a year securities underwriting is also conducted outside of platforms under the ECSPR without a prospectus, under the AltFG, or using a simplified Schedule D prospectus in accordance with Article 12 para. 3 KMG 2019 (and therefore making under an exemption from a prospectus pursuant to Article 1 (2) lit. (c) point (ii) ECSPR).

For every issue, the issuer must therefore remain aware of what issues they have already made during the last 12 months. Issues of securities up to EUR 5 mn per year, that are either issued without a prospectus under AltFG or using a simplified prospectus under Schedule D pursuant to Article 12 para. 3 KMG 2019, shall in any case count towards the calculation of the EUR 5 mn threshold under the ECSPR. For example, if during the last 12 months prior to using a platform under the ECSPR EUR 1 mn of securities have been issued without a prospectus under the AltFG and EUR 2 mn under a simplified prospectus under Schedule D under the KMG 2019, then the issuer shall only be allowed to issue a further EUR 2 mn in crowdfunding offers (securities and loans) on a platform under the ECSPR. Conversely, crowdfunding offerings on platforms under the ECSPR are also to be calculated in the limits for Schedule D prospectuses pursuant to Article 5 para. 3 (for investments) and Article 12 pars. 3 KMG 2019 (for securities). The issuance of investments on the other hand does not count towards the thresholds set out in the ECSPR.

Previously it was possible to offer up to EUR 2 mn per year in investments (e.g. participation rights, qualified subordinated loans of AltFG platforms and up to EUR 2 mn in securities without a prospectus. Since the entry into force of the ECSPR, the intermediation of transferable securities on Internet platforms of under EUR 5 million is generally restricted to licensed crowdfunding service providers. In the remaining scope of application of the AltFG (i.e. also when offering securities outside of a platform) only an information document under the AltFG needs to be drawn up, that is scrutinised by a tax adviser, attorney etc., filed at the Verein für Konsumenteninformation (VKI) and made available to investors. In addition it must be ensured that all AltFG issuance of an issuer and issuances under simplified Schedule D prospectuses, all offerings of securities that are exempted under the EU Prospectus Regulation in another EU Member State as well as crowdfunding offerings on platforms under the ECSPR over the course of a period of one year in total shall not be allowed to exceed the amount of EUR 5 mn, otherwise an investment prospectus must be drawn up for investments, and a prospectus under the EU Prospectus Regulation for securities. Moreover, over a period of seven years the outstanding (i.e. not yet repaid) amount of all moneys received from the issuance of investments under the AltFG shall not be allow to exceed EUR 5 mn, otherwise the corresponding prospectus is required to be drawn up.

All public offerings and non-public offerings of securities and investments in Austria are generally required pursuant to Article 24 KMG 2019 to be filed in the New-Issue Calendar that is administered by the OeKB’s notification office. This reporting obligation specifically does not apply for certain issuances outside the scope of application of the EU Prospectus Regulation as well as certain issuances under the Regulation that are exempted from the requirement to publish a prospectus.

It is important in this context that in the in the Supplementary Act on the Implementation of the ECSPR that issuances of securities and investments under the KMG 2019 of under EUR 2 mn per year are excluded from the reporting obligation. Securities offerings that are offered via platforms under the ECSPR as also not required to be filed with New-Issue Calendar, since according to the Supplementary Act the KMG 2019 does not apply for crowdfunding offerings within the scope of application of the ECSPR.

In the event of a breach of the obligation to publish a prospectus, the FMA may impose severe administrative penalties when securities (maximum fine EUR 700,000) or investments (maximum fine EUR 100,000) are publicly offered without an orderly prospectus. Furthermore, an announcement is also made on the FMA website, that a fine and its amount has been imposed against a specific person for such a breach.

Information about the procedure and costs of approving a prospectus can also be found here as well as in the Information on our website about capital market prospectuses.